1) towards full-scale industrialisation and inclusive growth the dti Customer Contact Centre: 0861 843 384 Website: www.thedti.gov.za

2) © Department of Trade and Industry, April 2015. The Business Process Services Unit of the Industrial Development Division the dti Campus 77 Meintjies Street Sunnyside Pretoria 0002 the dti Private Bag X84 Pretoria 0001 the dti Customer Contact Centre: 0861 843 384 the dti Website: www.thedti.gov.za

3) Contents 1. Acronyms............................................................................3 2. Executive Summary............................................................4 3. Introduction.........................................................................7 4. An economic imperative for BPS sub-sectors ................8 4.1. Economics that underpins Offshoring and Outsourcing... 9 5. Risks of Offshoring and Outsourcing.............................11 5.1. Offshoring criticism......................................................... 12 10. Alternative Offshore destinations: Global outlook........24 10.1.The best offshore location: Key indicators ....................... 25 10.2. Costs ............................................................................. 26 10.3. Skills............................................................................... 26 10.4. Environment .................................................................. 27 10.5. Quality of infrastructure ................................................. 27 10.6. Risk profile ..................................................................... 27 10.7. Market potential ............................................................. 28 11. Overview of SA’s economic profile.................................28 6. Dynamics of South Africa’s labour market....................14 11.1. Country’s progress in BPS............................................. 28 6.1. Impact of BPS Incentive Scheme and employment opportunities................................................................... 15 11.2. Global Competitiveness Index........................................ 29 6.2. Monyetla Work-Readiness Programme.......................... 16 12. Provincial economic indicators.......................................30 12.1. Western Cape................................................................. 30 7. Potential for investment attraction.................................18 8. Telecommunication: A key infrastructural factor in destination’s competitiveness........................................19 9. Beyond outsourcing to robotic automation...................20 9.1. Cloud computing............................................................ 21 12.2. KwaZulu-Natal................................................................ 32 12.3. Gauteng ......................................................................... 33 13. Summation........................................................................34 14. References........................................................................35

4) 2

5) 1. Acronyms BPS Business Process Services BPO Business Process Outsourcing DoC Department of Communications EDS Electronic Data Systems GDP Growth Domestic Product IP Intellectual Property IDC Industrial Development Corporation IPAP Industrial Policy Action Plan IPSF Industrial Policy Support Fund ITO Information Technology Outsourcing KZN KwaZulu-Natal LPO Legal Process Outsourcing OECD Organisation for Economic Co-operation and Development RBIDZ Richards Bay Industrial Development Zone SADC Southern African Development Community SETA Sector Education and Training Authority SSC Shared Services Centre the dti The Department of Trade and Industry WEF World Economic Forum 3

6) 2. Executive Summary In this third edition of the Annual Business Process Services (BPS) sector profile, the BPS sector desk, with the assistance of the provinces, compiles, prepares, highlights and disseminates information specific to the development of the sector and the challenges experienced from both the domestic and global perspectives. and offshore to third parties. The global economic downturn of the past six years has had a lingering effect on the growth of the global Growth Domestic Product (GDP) and associated employment opportunities. Yet, global revenues in the BPS market have grown due to the emergence of alternative, credible and low-cost BPS offshore destinations, including the ever-expanding, innovative types of services outsourced to third parties. The focus of Firstly, the report examines the underlying economics the global industry is increasingly shifting from the of the outsourcing and offshoring of business narrow, basic outsourcing advantages of cost and services, including associated opportunities and risks, talent to higher, value-added services, innovation and as a major global trend that has a significant positive transformation. Global sourcing is evolving from one impact on emerging economies with the required that is simply tactical to being of strategic benefit to skills, cost advantage and infrastructure. This growth the parties of the transaction. opportunity has been exploited by successful global players, such as India and the Philippines. Secondly, the report examines the domestic labour dynamics of the sector and the overall The industry, however, evolves quickly, with multinationals finding new areas to outsource 4 economic picture of the country since the onset of the economic crisis, which continues to shape how

7) global businesses respond to the increasing need to aspects of the processes, particularly where focus on maximising efficiency and hence the global outsourcing and offshoring results in job losses in outsourcing of non-core processes to emerging developed economies. Ordinarily, employment is locations. In addition, the report focuses on how South a key issue for any responsible government, and Africa re-aligns and reinforces its standing as one of helping workers who lose their jobs is a priority. This the leading offshoring locations, considering that the includes increased business trends of automation country’s contact centre market is well-established and the use of cloud computing to minimise the and highly sophisticated in terms of technology costs of inefficiencies and labour. In summary, this adoption and services offered. South Africa’s work- speaks to the risks, advantages and disadvantages readiness programme and sector-specific incentive of the maturity and unintended consequences of scheme have been commendable achievements as globalisation and the interdependence of world part of the country’s value proposition. This section economies. The public outcry from source markets will also highlight the uneven growth and comparative concerns the perceived redundancy of acquired skills advantages of regional economies as far as sector and knowledge of the workforce. Furthermore, trade development is concerned. theory economists and management analysts have Thirdly, the report analyses the global outsourcing and offshoring of business services, with particular challenged the previously assumed mutual benefits of offshoring business operations. focus on the growing public scrutiny. Much of the public debate has tended to focus on the negative 5

8) 6

9) 3. Introduction The BPS sector has been identified in the Industrial Policy Action Plan (IPAP) as having the potential to contribute towards accelerated job creation and attract foreign direct investment (FDI), if the necessary support is provided. The South African Government provides support to the sector mainly from an offshoring perspective as it capitalises on the growing global market, which leads to demand for risk minimisation through location diversification by global multinationals. In the 2014/15 financial year, the Department of Trade and Industry (the dti), in partnership with Process Outsourcing (LPO) and Shared Services Centres (SSCs). The purpose of the study was to formulate a business case and strategy for the support of the identified sub-sectors so as to further stimulate economic growth and employment creation. It further analyses regional industrial development for the sector in order to identify each region’s competitive and comparative advantage. The object is to enable the provinces to have unique value propositions that complement and is within the context of the unique South African Value Proposition. A review of the BPS sector strategy is under way in the 2014/15 financial year. the Industrial Development Corporation (IDC) through the Industrial Policy Support Fund (IPSF), commissioned a detailed sector-specific study on two BPS sub-sectors with the potential for leveraging and enhancing the country’s BPS sector, namely Legal 7

10) 4. An economic imperative for BPS subsectors A firm is considered to be the strategic locus within which organised human capital manufactures new products and business processes, thereby advancing the productivity of nations. In turn, industries and sectors form the basic economic units of a nation’s competitiveness in the international trade. Various critical factors influence the nature and patterns of international trade, for instance, the impact of capital flows and involvement of transnational corporations. The practice of global multinationals outsourcing and offshoring production and services has become common in a wide range of industries. This represents a significant change from the past prevalent practice of vertical integration in the organisation of production, which occurred throughout most of the 20th century. Innovation in business processes is the result of the implementation of best 8

11) practices as well as the search for “next practices” 4.1. Economics that underpins Offshoring and to push an organisation and its services to the Outsourcing next level. According to estimates, the value of In the main, offshoring and outsourcing entails outsourcing contracts has surpassed $100 billion per the organisational and technological ability year since 2004 (Everest Group, 2014). to relocate specific tasks and co-ordinate a geographically dispersed network of It is imperative to continuously examine the barriers activities. It decouples the linkages between to meaningful economic participation as well as the economic value creation and geographic variables that influence the potential growth of the BPS location. The result is the creation of global sector. In-depth analysis of the identified sub-sectors, commodity markets for particular skills and a LPO and SSCs, will enable informed participation by shift in the balance of market power among the industry and allow for exploitation of the economic firms, workers and countries. Traditionally, potential of the sector to attract investment and create offshoring is defined as the relocation of employment opportunities. This necessitates an business processes, including production, analysis of the potential economic value-add that can distribution and business services as well be derived from these sub-sectors, i.e. the contribution as core activities such as research and to GDP, potential job creation, and additional and development, to lower-cost locations outside indirect job creation potential, which could emanate national borders. The economic rationale is to from the value chains. reduce the cost implications of managing non9

12) core functions, yet the transfer of information the foundation of modern transaction cost creates a certain level of risk. To mitigate economics. the inherent risks, a considerable degree of two-way information exchange, co-ordination The concept of outsourcing, particularly and trust is essential. Conventionally, the in the Information Technology sector, was outsourcing business is characterised by popularised by Ross Perot when he founded expertise that is not present in the core of the Electronic Data Systems (EDS) in 1962. client organisation. He is famed to have told a prospective client that “You are familiar with designing, The theoretical foundation of the economics manufacturing and selling furniture, but we’re of outsourcing was first established by Ronald familiar with managing information technology. Coase in1937 when he asked the question, We can sell you the information technology “What establishes the boundaries of a firm?” you need, and you pay us monthly for the A comparison of the costs of the internal service with a minimum commitment of two to supply of a particular task or service with the 10 years.” external market costs of the same task or service helps to determine the efficiency of internal or external production. By establishing transaction cost calculation, Coase laid 10

13) 5. Risks of Offshoring and Outsourcing There are a number of challenges and risks associated with offshoring and outsourcing. Many potential and existing offshore destinations are associated with certain location-specific risks that multinational investors balance against expected cost savings. Investors use business intelligence and strict evaluations of country value propositions as well as medium- to long-term marketing strategies of competing countries when making decisions around geographic location. Cost savings that make a particular location attractive at one point in time are sometimes significantly reduced by new tax regimes, exchange-rate volatility and rapid increases in local wage rates. As a result, multinationals opt for vendor diversification and alternative offshoring destinations. Accordingly, multinationals attempt to balance high potential returns against higher country-specific risks that depend on potentially shifting political, regulatory and economic conditions. This results in intense competition between emerging alternative offshore destinations in terms of concessions and incentives offered, which often causes the deterioration of respective domestic labour laws, in turn leading to highly confrontational industrial relations and public outcry from civil society and domestic market participants. Similarly, the equation of corporate profits and national wealth is misplaced on economic grounds and ideological in its universalisation of corporate interests. The offshoring of services provides recipient countries with substantial employment opportunities. However, workers in these industries and occupations increasingly require higher skills competencies and higher incomes than workers in the manufacturing 11

14) and other non-tradable service activities. As a result to multinationals’ attempts to avoid what they there is contention that offshoring is not necessarily perceive as burdensome company tax. Similarly, about mutual trade benefit, with some economists the recipient countries contribute to the problem and management scholars arguing that reducing by inadvertently signing away their tax revenue wages through offshoring leads to wealth creation because of weak domestic policies and ill-conceived for shareholders, but not necessarily for countries tax incentives to attract investment through offshore and employees, and that many displaced workers business operations. The accepted notion is that have difficulty “trading up” to higher skilled jobs. incentives drive investment choices without asking Research conducted by Jensen and Kletzer (2006) whether business can operate efficiently and prior to the global recession showed that tradable sustainably without incentives in the long run. industries experienced a higher rate of job loss than non-tradable industries, with the greatest difference outside of manufacturing. In addition, a discomforting level of job insecurity is associated with employment in tradable activities, including services. A neglected, if not overlooked, issue is the impact of financial harm experienced by offshore destinations in the form of profit shifting and base erosion relating 12 5.1. Offshoring criticism Global offshoring and sourcing might be perceived as an irreversible megatrend, but is politically controversial in source markets. The backlash, particularly against the offshoring of IT in countries such as the United States and Australia, is based on the notion that the practice results in job losses. Global discourse

15) contends that offshoring signals a new include software engineering and ICT-related structural development in the global political business processes. This has resulted in a economy, one that raises concerns not only backlash from politicians, pressure groups and for the competitiveness of countries, but also organised labour in the developed markets, for the welfare of large groups of workers. which is likely to impact on opportunities for job creation in emerging offshore destinations. The previous wave of material offshoring, predominantly in source markets such as the US and the United Kingdom, primarily affected low-skill intensive components of production and services. This time around, however, the picture is different with skilled labour increasingly producing business services. In many developed countries, the tradability raises concerns that while previously low-skilled labour was substituted by cheap imports of intermediates, it is now skilled labour that is likely to suffer a decline in demand. Most popular examples 13

16) 6. Dynamics of South Africa’s labour market Unemployment and the shortage of certain skill sets in the BPS sector, particularly at management and supervisory levels, are two of many challenges facing our country. South Africa continues to struggle with a structurally high unemployment rate, which is currently estimated at more than 20, 0% and registered 25, 2% in the first quarter of 2014. According to the HIS Country Risk report on South Africa, the country’s economy was only able to create about 460,000 jobs per year during the five-year period preceding the recession of 2009, which clouds prospects for employment creation in the current slow growth environment. South Africa’s unemployment is deeply rooted in structural problems, including a lack of appropriate skills, which has kept unemployment high despite stronger economic growth in the pre-2009 global 14

17) recession years. Labour absorption in some Incentive Programme was first launched national sectors of the economy has been negligible in July 2007 to assist in attracting vital when compared to the services sector. This is not investment and reduce the cost gap between surprising, given the dominance of the services the country and its competitors. The scheme sector not only in the domestic economy, but also has been a catalyst to the growth of the globally. Statistics SA estimates that the labour force offshore BPS industry in South Africa. It grows annually by between 500,000 and 700,000 job underpins the country’s value proposition by seekers. Meanwhile, the unemployment rate among making South Africa increasingly attractive the youth increased from 33% to 36% between when compared to other countries competing 2008 and 2014. In addition, the youth accounted for for offshored business operations. Its approximately 64% of the working-age population, existence has contributed to the creation but are under-represented in employment, accounting of approximately 9,000 jobs, with a growth for a mere 49%. rate of 26% per annum from 2011 to 2014. According to the Everest Group report, 6.1. Impact of BPS Incentive Scheme and 2014, the UK is South Africa’s largest source employment opportunities market for offshored business operations The BPS sector is considered a key sector for attracting investment and job creation. The Business Process Outsourcing (BPO) and employs more than 18,000 people. A key recommendation of the report is that the incentive programme be continued beyond its 15

18) current three-year duration (2011-2014) so as and 3,000 in the third phase. The recently to drive long-term competitiveness and growth completed phase (2013-2014) trained more of the sector. than 3,233 learners. The participation of key stakeholders ensures the programme creates 6.2. Monyetla Work-Readiness Programme The Monyetla Work-Readiness Programme was designed to accelerate training for entry-level jobs within South Africa’s growing BPS industry and established in response to the shortage of skills in the sector. The intent from outset was to provide extensive theoretical and practical training over the 16-week course, which includes 160 hours of call centre experience. Monyetla targets school leavers, unemployed graduates, women, disabled people and youth between the ages of 18 and 35 years. Since inception, the programme has benefitted 1,307 people in the pilot phase, 3,350 in the second phase 16 a talent pool of skills required for efficient operations in their variable services offerings and line functions. The programme curriculum is designed to align with the Sector Education and Training Authority (SETA) and covers the essential skills required to enter into the BPS sector. A minimum of 68 credits of the relevant skills programmes at NQF Level 3 and above is required, and the training providers, assessors and moderators must be registered with one of the following SETAs: INSETA, FASSET, BANKSeta, MICTS or Services SETA.

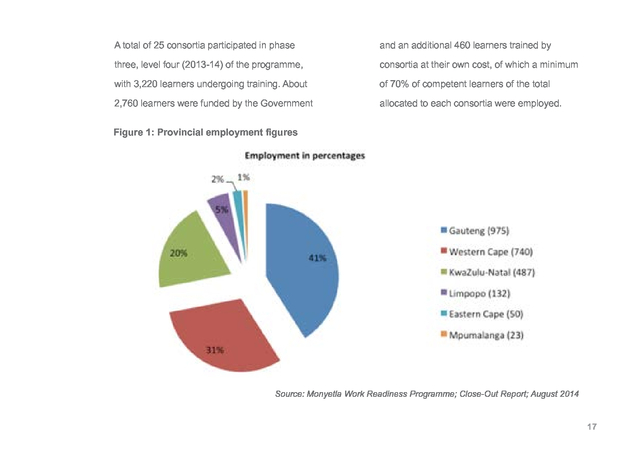

19) A total of 25 consortia participated in phase and an additional 460 learners trained by three, level four (2013-14) of the programme, consortia at their own cost, of which a minimum with 3,220 learners undergoing training. About of 70% of competent learners of the total 2,760 learners were funded by the Government allocated to each consortia were employed. Figure 1: Provincial employment figures Source: Monyetla Work Readiness Programme; Close-Out Report; August 2014 17

20) 7. Potential for investment attraction In this unpredictable global economic environment, trade and investment opportunities to drive economic growth are hindered by the triple challenge of poverty, inequality and unemployment, which is not unique to South Africa’s socio-economic circumstances. A country needs to have credible dynamic skills sets, feasible business incubation, training and development programmes, appropriate investor support and functional mentoring processes for emerging enterprises in the concerned sector if it plans to increase its chances of attracting investment opportunities for meaningful development. The proposed relaxation of a number of crossborder financial regulations and tax requirements on companies within the Southern African Development Community (SADC) will make it easier for banks, financial institutions and foreign companies to invest 18

21) in regional countries neighbouring South Africa and The policy intent is to address the lack of access will reinforce South Africa’s position as a gateway to to high-speed and good-quality bandwidth not the continent, in spite of it losing the tag of being the only to business, but also to public institutions largest economy in Africa to Nigeria. and the broader society. For instance, the City of Johannesburg has taken over from the private entity 8. Telecommunication: A key infrastructural factor in destination’s competitiveness the commercial operations of the broadband network for the city to speed up the roll out and availability of the network. In addition, the Gauteng and Western Voice, data and broadband services and product Cape provincial governments plan to invest R1.2 prices are critical to the growth of the BPS sector. billion and R3 billion respectively over the next three South Africa has achieved significant policy to five years in rolling out broadband connectivity milestones to transform the regulatory regime to across provinces. create a cost-competitive telecommunications sector. This includes undersea cables, availability of Telecommunication costs are critical in terms of broadband connectivity and the much-delayed digital infrastructural affordability and availability. For migration process. instance, the Philippines had early deregulation of the telecoms sector, which markedly pushed down The Department of Communications released its bandwidth costs by approximately 40%. According the national broadband policy in December 2013. to research conducted by the World Economic 19

22) Forum (WEF), good broadband internet access contributes between 0, 25% and 1, 4% to a country’s to consistently seek out efficient ways to drive down economic growth. This demonstrates how a proactive costs and improve productivity. The concern is that government can quickly change the offshore cost the traditional value drivers for application services equation. Prior to the political turbulence in Egypt, the are unable to effectively generate incremental value. cost of power, telecommunications and internet were Furthermore, recent advances in information and among the lowest; lower than in some European communication technologies have gained economy- and Asian countries. For South Africa, the gap has wide importance, raising concerns that neither narrowed considerably over the last five years and is services nor high-skilled labour might be sheltered anticipated to be reduced by approximately 20% over from international competition, but increasingly the next coming three years. 9. reduced management costs. The economic motive is susceptible to offshoring. Beyond outsourcing to robotic automation A new era of intelligence is propelling businesses to go beyond business process offshoring by leveraging Global sourcing standardisation and rigorous application support have been the focus in a manner similar to the creative destruction that is application outsourcing over the past decade. A occurring in the IT field. Creative destruction refers closer look at IT applications portfolios shows that to the incessant product and process innovation many businesses aspire for greater agility and 20 automation and analytics to advance their profits, in mechanism by which new production units replace

23) out-dated ones. An adoption of next-generation programs used to automate business activities such technologies and automation is enabling enterprises as accounts payable and receivable, transaction to achieve effective application rationalisation, cutting processing and order management. The robotic across the entire IT function. This enables enterprises process automation is relatively new and there is few to free up a significant chunk of their IT budget, bona fide case studies to showcase a completely the majority of which is currently dedicated to core convincing necessity. Yet, increasingly providers are operations, maintenance and support systems. starting to experiment with the concept. The efficiency of decisions around the use of robotic 9.1. automation not only depends on managerial talent, but also on the existence of sound institutions that provide a proper transactional framework. At the microeconomic level, restructuring is characterised by countless decisions to create and recreate production arrangements. These decisions are often complex, involving multiple parties as well as strategic and technological considerations. Robots are at the centre of today’s business process automation revolution, where they take the form of software Cloud computing Cloud, or a hosted and managed server solution, is considered a significant leveller in business efficiency and growth within the IT domain. It is believed to allow even small and medium-sized enterprises (SMEs) to access hardware and the latest software platforms that were previously the preserve of big corporate business. It implies low initial cost as there is no major upfront investment in hardware and software. Accordingly, 21

24) companies benefit from better cash flow in contact centres shows that cloud computing and are able to allocate their IT staff to more is gaining significant preference over the strategic projects. The upgrades are managed latter. As business and customer requirements seamlessly, allowing users to enjoy the new have become more complex, the on-premise features almost absolutely free. technology still used in many contact centres has become equally more complex. Industry analysts contend that contact centres are not just moving to the cloud to take For example, a Kenyan tech firm, Uhasibu, advantage of its breakthrough in technology focuses on developing cloud-based and reliability, but also because it is a smart accounting systems that focus on local market choice for the future of enterprises. They systems, and is capitalising with its latest argue that the key to moving contact centre application MiniERP. operations to the cloud lies in a vision of future plans for overall business. Additionally, it is about having realistic expectations targeted specifically at retail-based SMEs in for growth and operational diversity. A East Africa. It addresses the “operational” side comparative analysis of the functionality of of a business by providing a way to record cloud technology and conventional premise- financial accounting information without based solutions for technology management 22 MiniERP is a cloud-based ERP solution, requiring employees of SMEs to have the

25) financial training or knowledge of how to use models such as Saas and cloud, they a full accounting system. In cases of internet continue to be challenged by effectively connection failures, the package is still leveraging these models to derive meaningful accessible due to its offline capability. business value and are looking to service providers to help them achieve these goals, The demand to manage this kind of driving up inclusion of consulting in Application communication technology is much greater, Outsourcing contracts. In sum, cloud as are the demands to ensure stability, computing is an ideal way forward for firms reliability and resiliency. The proponents that have ageing infrastructure to avoid and of cloud computing argue that, from a minimise costs associated with infrastructural strategic perspective, a cloud-based solution overhaul. offers an intelligent monitoring, dedicated support resource, on-going management, and formalised security architecture and processes. They further contend that cloud assures business continuity and disaster recovery capabilities for contact centres operations. Although enterprises are aware of and increasingly adopting new delivery 23

26) 10. lternative Offshore destinations: Global A outlook Emerging economies have made significant traction in terms of penetrating markets and making their presence known as possible offshore destinations. This is largely due to emerging sourcing destinations making significant efforts to differentiate themselves from others. The industry has matured and so have the considerations and factors that influence decisions on location moved beyond low-cost outsourcing concerns. For example, Egypt is promoting itself as a low-cost destination for call centres that specialise in European languages and offers a large pool of university graduates to Western companies through special industry-university partnerships. Dubai and Singapore present their IT security and legal systems to the outsourcing of high-security and business-continuity services. The Philippines stresses its excellent English skills to 24

27) attract English-speaking call centres. Morocco is enjoyed by India is its management skills, which most trying to attract French-speaking European clients to emerging sourcing destinations are unable to offer. set up call centres, while Central and South American Spanish-speaking countries hope to establish call Accordingly, South Africa cannot expect multinational centres to provide services to the Hispanic market in companies to invest in the country as part of their the US. social responsibility demands. Multinationals have a “wish list” of requirements to operate successfully India continues to dominate and maintain leadership in any country, including stable electricity supply in Information Technology Outsourcing (ITO) and and a well-educated workforce. To maintain the BPO services. Many large multinational companies momentum and remain on the global radar, South hold the view that India is a centre of excellence for Africa needs to work intelligently and be strategically ITO and BPO, and not merely a low-cost destination. organised to realise the gains and achievements The US and European multinationals continue to of the last couple of years and focus on continuous engage Indian suppliers for technical services such relevant improvements to remain globally competitive as programming and platform upgrades. However, and offset the superfluous costs of the geographic as this relationship matures, they are gradually location. assigning Indian companies with more challenging work, such as development and support tasks for critical business applications. Another advantage 10.1. The best offshore location: Key indicators The split between onshore and offshore 25

28) outsourcing is difficult to determine with any degree of precision. However, a feasible and convenient way to approach this phenomenon is to look at it from the supply side. India is known to be the principal offshore vendor of IT services, claiming at least 80% of the world’s business. India’s software and IT-enabled services export industry achieved annual growth of about 62,3% between 2002 and 2006 before being interrupted by the global recession in 2007. Conventionally, six key indicators are considered to be key assessment criteria that influence the decisions of multinationals around choice of geographic location. The assessment criterion is not listed in order of any particular importance as companies have different strategic and operational objectives: 26 10.2. Costs • Labour costs: Average wages for skilled workers and managers. • Infrastructure costs: Unit costs for telecom networks, internet access, power and office rent. • Corporate taxes: Tax breaks and regulations, and other incentives for local investment. 10.3. Skills • Skill pool: The size of the labour pool with required skills. This may entail skills such as technical and business knowledge, management skills, languages and the ability to learn new concepts and innovate. In addition, the scalability of labour resources in the long term, that is, the ability to supply sufficient labour resources to handle growing demand, is a major issue that is considered when choosing an offshore destination. An indication of the scalability of

29) labour resources in a country is the growth in the number of graduates with desired skills. Countries that offer scalability of labour resources are also more likely to keep wages relatively low due to the constant supply of new graduates. • Vendor landscape: The size of the local sector providing IT services and other business functions. It is imperative to evaluate the landscape in terms of the general skills set (capabilities and competencies). 10.4. Environment • Governance support: Policy on foreign investment, labour laws, bureaucratic and regulatory burden, level of corruption. • Business environment: Compatibility with prevailing business culture and ethics. • Living environment: Overall quality of life, health standard and health-related prevalence of infections, and serious crime per capita. • Accessibility: Travel time, flight frequency and time difference. 10.5. Quality of infrastructure • Telecommunications and IT: Network downtime, speed of service restoration and connectivity. • Real estate: Availability and the quality, including rental costs. • Transportation: Scale and quality of road and rail networks. • Energy: Reliability of power supply. 10.6. Risk profile • Security issues: Risks to personal security and property-related issues such as fraud, crime and terrorism. • Disruptive events: Risk of a labour uprising, political unrest and natural disasters. • Regulatory risks: Stability, fairness and efficiency of the legal framework. 27

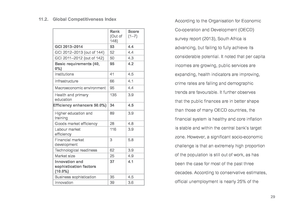

30) • Macroeconomic risks: Cost of inflation, currency fluctuation and capital freedom. • Intellectual property (IP) risk: Strength of the data and IP protection regime. 10.7. Market potential • Attractiveness of the local market: Current GDP and its growth rate. • Access to nearby markets, both in the host country and the adjacent region. According to The Global Competitiveness Report (2013-2014), South Africa continues to be considered one of the preferred offshore destinations in Africa, even though it has not yet returned to its pre-crisis growth rates. In market efficiency, it fares relatively well and is ranked in the top 20 in financial market development, with Mauritius and Kenya. The country’s technological uptake continues to show positive signs of upward mobility and featured in the top half of the overall GCI rankings. 11. Overview of SA’s economic profile South Africa is one of the most stable economies on 11.1. Country’s progress in BPS the African continent. It is a middle-income country Population (millions).................................50.6 with a fully developed basic infrastructure. The GDP (US$ billions) .................................384.3 country exhibits several indicators of a developing GDP per capita (US$).............................7,507 economy, such as well-grown primary, secondary and GDP (PPP) as share (%) of world total..... 0.70 tertiary sectors and non-dependency on agriculture. The manufacturing, mining and service sectors are the largest contributors to the country’s GDP. 28

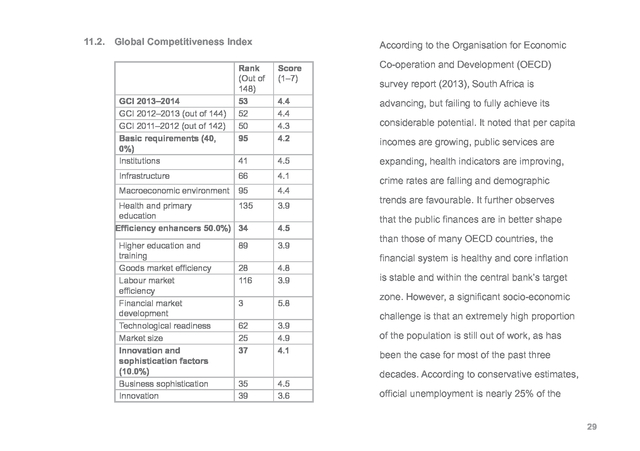

31) 11.2. Global Competitiveness Index GCI 2013–2014 GCI 2012–2013 (out of 144) GCI 2011–2012 (out of 142) Basic requirements (40, 0%) Institutions According to the Organisation for Economic Co-operation and Development (OECD) Rank (Out of 148) 53 52 50 95 Score (1–7) 4.4 4.4 4.3 4.2 advancing, but failing to fully achieve its survey report (2013), South Africa is considerable potential. It noted that per capita incomes are growing, public services are 41 4.5 expanding, health indicators are improving, Infrastructure 66 4.1 Macroeconomic environment 95 4.4 crime rates are falling and demographic Health and primary 135 education Efficiency enhancers 50.0%) 34 Higher education and training Goods market efficiency Labour market efficiency Financial market development Technological readiness Market size Innovation and sophistication factors (10.0%) Business sophistication Innovation 3.9 4.5 89 3.9 28 116 4.8 3.9 3 5.8 62 25 37 3.9 4.9 4.1 35 39 4.5 3.6 trends are favourable. It further observes that the public finances are in better shape than those of many OECD countries, the financial system is healthy and core inflation is stable and within the central bank’s target zone. However, a significant socio-economic challenge is that an extremely high proportion of the population is still out of work, as has been the case for most of the past three decades. According to conservative estimates, official unemployment is nearly 25% of the 29

32) workforce. South Africa’s economic policy is with Gauteng second. Kwazulu-Natal has the largest firmly focused on controlling inflation. The number of agents servicing the offshore market. country, however, has had significant budget deficits that restrict its ability to deal with pressing economic problems. 12. Provincial economic indicators BPS growth and maturity and the preference of global investors is still largely concentrated in the three country’s metropolitan cities, namely Cape Town (Western Cape), Johannesburg (Gauteng) and Durban (KwaZulu-Natal). However, Port Elizabeth (Eastern Cape) is increasingly emerging as a preferred metropolitan city, with new offerings in its value proposition, including infrastructural improvements, as well as the commitment of the provincial government and support of national Government. The Western Cape has a significant number of operators servicing the offshore market, 30 12.1. Western Cape The Western Cape BPS industry continues to enjoy the support of government at all levels, with companies accessing the support of the Department of Trade and Industry’s (the dti) BPS incentive scheme as well as the Monyetla programme. The outsourcing sector constitutes 50% of the market, a 6% increase from 2013, with the captive market also contributing 50%. The sector added 1,537 offshore servicing jobs and grew in total by 8% to 41,000 jobs over the 2013/14 financial year. The financial services sector accounts for the highest proportion of agents in the industry at 41, 7%, a 0, and 5% increase from 2013,

33) with retail at 14, 9%, a decrease of 10%, organisations and powerful brands such and telecommunications at 12, 5%, a 2, 7% as Amazon, Asda and Shop Direct has increase from 2013. There is a growing focus contributed to growth in the retail sub- on the delivery of higher value, more complex sector; and BPS work from the region, such as legal • Telecommunication – Major telecoms process outsourcing and shared services. This brands from the UK and Europe are using will complement the already strong presence the province as a customer service base of voice-based services and allow outsourcers for their international clients. to offer a wider range of solutions to their clients from the Western Cape. Additionally, there is notable BPS activity in Financial Services (41,7%), Retail (14,9%), The province’s competencies and comparative Telecoms (12,5%), Legal (7,2%), IT (6,0%), advantages are underpinned by the following Public Sector (4,4%), Transport, (4,2%), sub-sectors: Energy (3,7%), Marketing (2,0%), Media • Financial services – large financial domestic captives headquartered and operating from Cape Town, complemented by a number of large financial outsourcers; • Retail – the presence of international (0,7%), Education (0,7%), Security (0,6%), Healthcare (0,4%) and Other (1,0%). There is growing capacity in the provision of back-office fund administration from both 31

34) South African companies such as Maitland largest industries in the manufacturing sector and international players like State Street. are automobile; wood, pulp and paper; This is well-aligned to the large insurance and chemicals and petrochemicals; and food asset management sub-sectors that operate in and beverages. The Richards Bay Industrial the region. The provincial strategy to support Development Zone (RBIDZ) now trades as the BPS sector will increasingly enable the a Special Economic Zone. The hotel and provision of these higher-value services. The tourism industries still influence the economic Western Cape government has shifted its landscape of the province, which continues focus to address the challenges around the to be one of the alternative locations for skills pipeline for the sector and intends to outbound sales campaigns servicing markets pilot a BPS skills development project in the in the UK and Australia. As a result, KwaZulu- near future. Natal considers itself to be the “Sales Hub” of the country and has a strong and unique sales 12.2. KwaZulu-Natal The provincial economy continues to be dominated by three industries, namely manufacturing; finance and business services; and wholesale and retail trade, including hotels and accommodation industries. The 32 ethic. In terms of location, most investments in the province are concentrated largely in eThekwini region, covering Durban Central Business District (“CBD”), Mount Edgecombe and

35) Umhlanga, followed by the UMgungundlovu telecommunications, and textile and retail (Pietermaritzburg) and iLembe (Stanger) services. districts. 12.3. Gauteng ICT and broadband distribution, including undersea cables, forms the backbone of most businesses in the province, given its geographic location of the Indian Ocean, and training on product-specific and basic customer service such as Career Box, Harambes and ISA (Impact Sourcing Academy) has emerged as the new subsector. Segmentation of the BPS industry by activity includes activities such as agricultural and retail services, banking and financial services, government/municipalities services, insurance, leisure and online gambling, Gauteng is the commercial capital of South Africa and a microcosm of the country’s economic structure. The provincial economy was originally driven by the mining sector, which provided a platform for growth in manufacturing, followed by tertiary sectors including trade and finance. It is both a commercial and industrial hub that encompasses the principal cities of Johannesburg and Pretoria. Pretoria is the administrative capital of South Africa and Johannesburg is the capital of Gauteng as well as the country’s largest metropolis and financial heart of the southern African subcontinent. Between the two cities is 33

36) Midrand, a prime growth point destined purposes, as demonstrated by the global awards as to become a city in its own right. Gauteng the location for offshored business operations (UK government’s New Growth Path is aligned and European awards). The UK remains the largest to the National Growth Path and has the offshore source market for South Africa. It accounts following pillars: for approximately 62% of offshore operations, with • Strategic Economic Infrastructure Development – industry and sector development • Tourism Development • Knowledge and Green Economies • SMME and Co-operatives Support and Local Economic Development 13. Summation South Africa continues to be on the global radar and remains a competitive alternative offshore destination. It is positioning itself as a preferred destination of high-value services for offshoring 34 Australia another potential source of offshored business functions. The South African market provides services for global customers, banking, financial and insurance services as well as online retailing, telecoms and media services.

37) 14. References AFK Insider. Original; Kenyan Accounting Software Firm Launches MiniERP for Startups. Kevin Mwanza, 25 August 2014. Business Day, 5 August 2014. Profit shifting ‘just a part’ of Africa tax loss. David L Levy. Offshoring in the New Global Political Economy. Journal of Management Studies 42:3 May 2005. University of Massachusetts, Boston Everest Group. 2014. Assessment of South Africa’s incentive programme and recommendations on revised incentives for Business Process Services. Final Report. The Department of Trade and Industry. (South Africa). Operational Agility Forum. Robotic Automation – What next for BPOs? Stefan Ried, Ph.D., Holger Kisker, Ph.D and Pascal Matzke. Vendor Strategy Professionals. The Evolution of Cloud Computing Markets IHS Economics and Country Risk Country Reports – South Africa; 3 June 2014 The Global Competitiveness Report, 2013–2014. Insight Report, World Economic Forum. Zhonghua Qu and Michael Brocklehurst. 2003. An analysis of the role of transaction costs in supplier selection. Journal of Information Technology, 18. 53-67 OECD Economic Survey: South Africa, OECD 2013 35

38) 36

39) 37

40) the dti Campus 77 Meintjies Street Sunnyside Pretoria 0002 the dti Private Bag X84 Pretoria 0001 the dti Customer Contact Centre: 0861 843 384 Website: www.thedti.gov.za towards full-scale industrialisation and inclusive growth the dti Customer Contact Centre: 0861 843 384 Website: www.thedti.gov.za