1) Captive Insurance Benchmarking The Bahamas

2) Contents Page Domicile comparison â– Travel cost and time analysis â– Summary of regulatory requirements and costs 2-3 4 Appendix â– The Bahamas 5 â– Bermuda 6 â– Cayman Islands 7 â– Vermont 8 â– Guernsey 9 â– Anguilla 10 â– Barbados 11 â– Nevis 12 â– British Virgin Islands 13 â– Isle of Man 14 â– Turks and Caicos 15 The Insurance Commission of The Bahamas 16 Bahamas Financial Services Board 17 KPMG 18 © 2014 KPMG, a Bahamas partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, (“KPMG International”) a Swiss entity. All rights reserved. 1

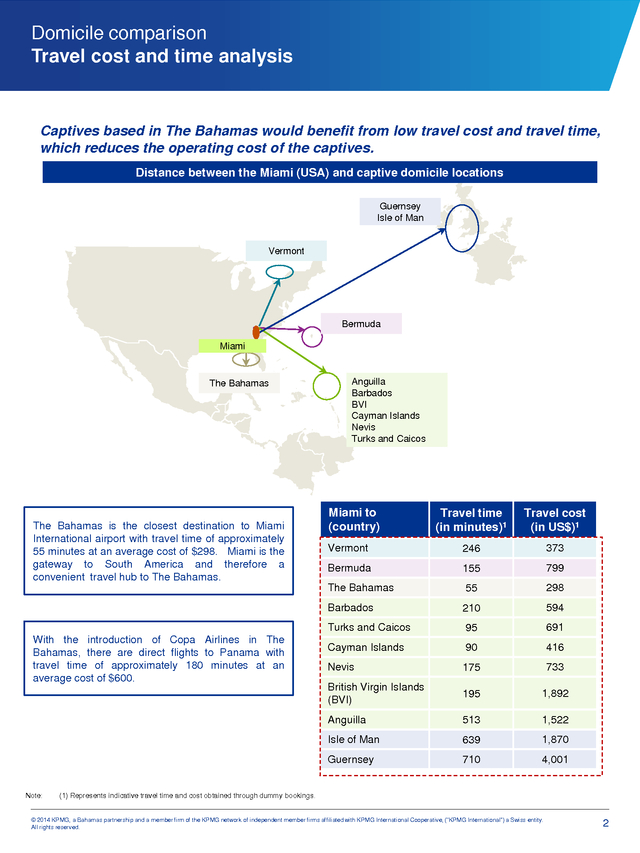

3) Domicile comparison Travel cost and time analysis Captives based in The Bahamas would benefit from low travel cost and travel time, which reduces the operating cost of the captives. Distance between the Miami (USA) and captive domicile locations Guernsey Isle of Man Vermont Bermuda Miami The Bahamas Anguilla Barbados BVI Cayman Islands Nevis Turks and Caicos Miami to (country) Vermont 246 373 Bermuda 155 799 55 298 210 594 Turks and Caicos 95 691 Cayman Islands 90 416 Nevis 175 733 British Virgin Islands (BVI) 195 1,892 Anguilla 513 1,522 Isle of Man 639 1,870 Guernsey Note: Travel cost (in US$)1 Barbados With the introduction of Copa Airlines in The Bahamas, there are direct flights to Panama with travel time of approximately 180 minutes at an average cost of $600. Travel time (in minutes)1 The Bahamas The Bahamas is the closest destination to Miami International airport with travel time of approximately 55 minutes at an average cost of $298. Miami is the gateway to South America and therefore a convenient travel hub to The Bahamas. 710 4,001 (1) Represents indicative travel time and cost obtained through dummy bookings. © 2014 KPMG, a Bahamas partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, (“KPMG International”) a Swiss entity. All rights reserved. 2

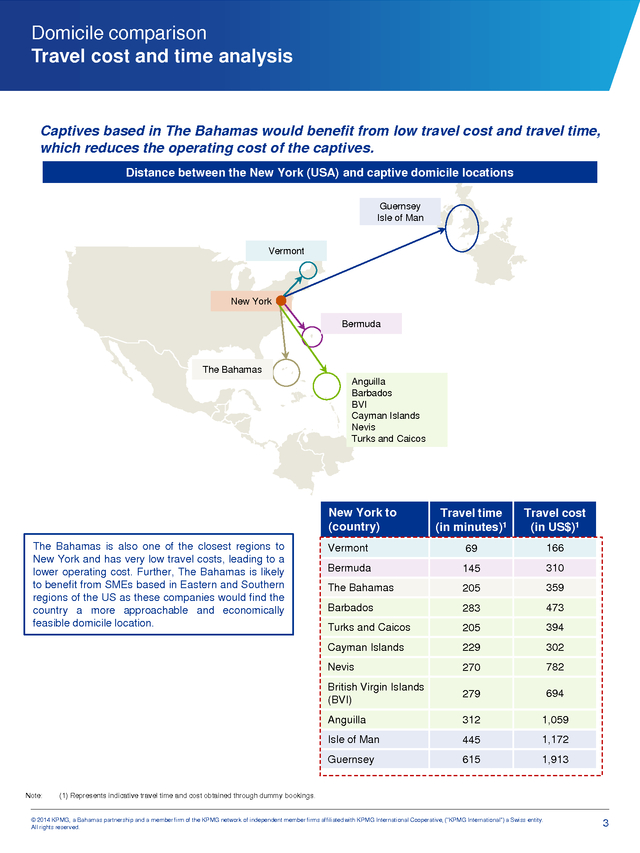

4) Domicile comparison Travel cost and time analysis Captives based in The Bahamas would benefit from low travel cost and travel time, which reduces the operating cost of the captives. Distance between the New York (USA) and captive domicile locations Guernsey Isle of Man Vermont New York Bermuda The Bahamas Anguilla Barbados BVI Cayman Islands Nevis Turks and Caicos New York to (country) Vermont 69 166 Bermuda 145 310 The Bahamas 205 359 Barbados 283 473 Turks and Caicos 205 394 229 302 Nevis 270 782 British Virgin Islands (BVI) 279 694 Anguilla 312 1,059 Isle of Man 445 1,172 Guernsey Note: Travel cost (in US$)1 Cayman Islands The Bahamas is also one of the closest regions to New York and has very low travel costs, leading to a lower operating cost. Further, The Bahamas is likely to benefit from SMEs based in Eastern and Southern regions of the US as these companies would find the country a more approachable and economically feasible domicile location. Travel time (in minutes)1 615 1,913 (1) Represents indicative travel time and cost obtained through dummy bookings. © 2014 KPMG, a Bahamas partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, (“KPMG International”) a Swiss entity. All rights reserved. 3

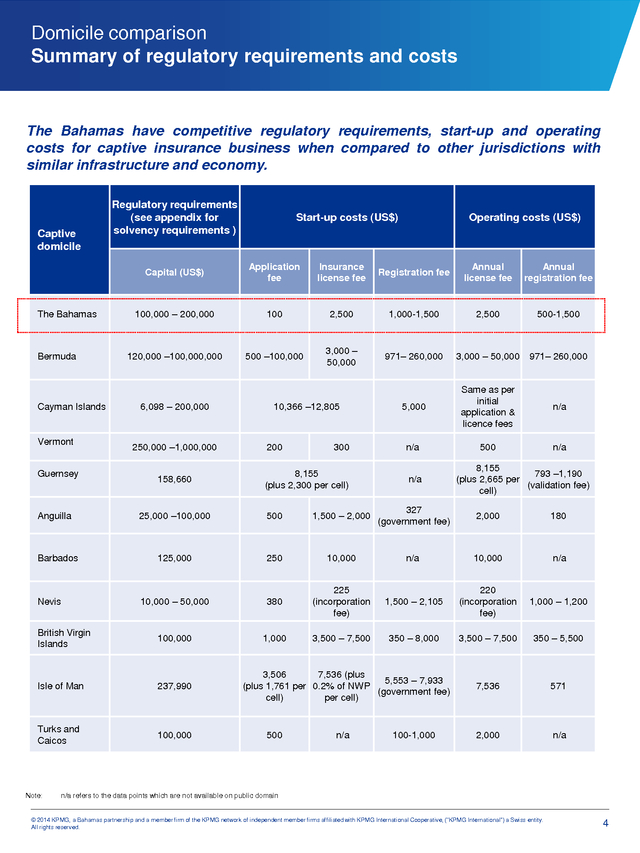

5) Domicile comparison Summary of regulatory requirements and costs The Bahamas have competitive regulatory requirements, start-up and operating costs for captive insurance business when compared to other jurisdictions with similar infrastructure and economy. Captive domicile Regulatory requirements (see appendix for solvency requirements ) Start-up costs (US$) Operating costs (US$) Capital (US$) The Bahamas Bermuda Cayman Islands Vermont Guernsey Application fee Insurance license fee Registration fee Annual license fee Annual registration fee 100,000 – 200,000 100 2,500 1,000-1,500 2,500 500-1,500 120,000 –100,000,000 500 –100,000 3,000 – 50,000 971– 260,000 3,000 – 50,000 971– 260,000 5,000 Same as per initial application & licence fees n/a 300 n/a 500 n/a 8,155 (plus 2,300 per cell) n/a 6,098 – 200,000 250,000 –1,000,000 158,660 10,366 –12,805 200 8,155 793 –1,190 (plus 2,665 per (validation fee) cell) 25,000 –100,000 500 1,500 – 2,000 327 (government fee) 2,000 180 125,000 250 10,000 n/a 10,000 n/a 10,000 – 50,000 380 225 (incorporation fee) 1,500 – 2,105 220 (incorporation fee) 1,000 – 1,200 British Virgin Islands 100,000 1,000 3,500 – 7,500 350 – 8,000 3,500 – 7,500 350 – 5,500 Isle of Man 237,990 7,536 571 Turks and Caicos 100,000 2,000 n/a Anguilla Barbados Nevis Note: 3,506 7,536 (plus 5,553 – 7,933 (plus 1,761 per 0.2% of NWP (government fee) per cell) cell) 500 n/a 100-1,000 n/a refers to the data points which are not available on public domain © 2014 KPMG, a Bahamas partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, (“KPMG International”) a Swiss entity. All rights reserved. 4

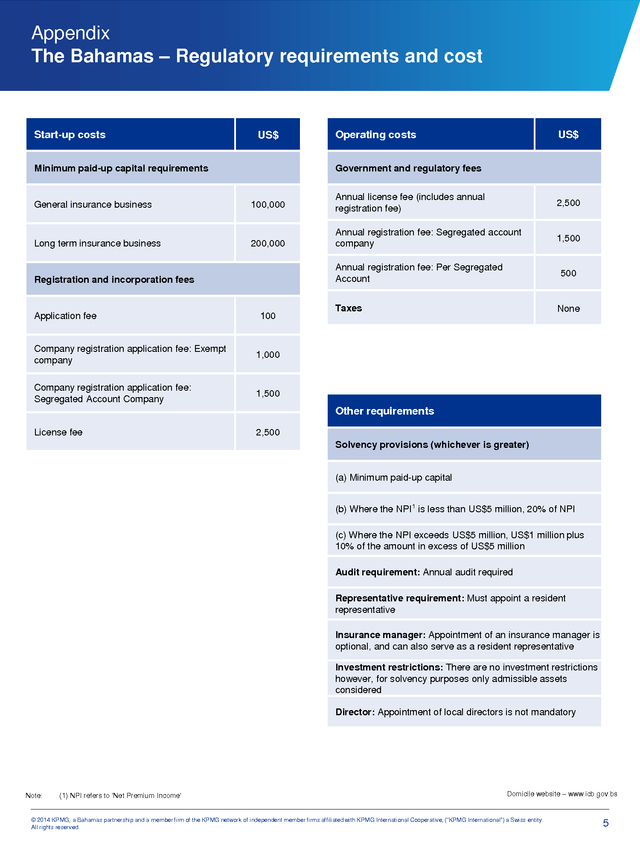

6) Appendix The Bahamas – Regulatory requirements and cost Start-up costs US$ Minimum paid-up capital requirements Operating costs US$ Government and regulatory fees General insurance business 100,000 Annual license fee (includes annual registration fee) 2,500 Long term insurance business 200,000 Annual registration fee: Segregated account company 1,500 Annual registration fee: Per Segregated Account Registration and incorporation fees Application fee 100 Company registration application fee: Exempt company Taxes None 1,000 Company registration application fee: Segregated Account Company 500 1,500 Other requirements License fee 2,500 Solvency provisions (whichever is greater) (a) Minimum paid-up capital (b) Where the NPI1 is less than US$5 million, 20% of NPI (c) Where the NPI exceeds US$5 million, US$1 million plus 10% of the amount in excess of US$5 million Audit requirement: Annual audit required Representative requirement: Must appoint a resident representative Insurance manager: Appointment of an insurance manager is optional, and can also serve as a resident representative Investment restrictions: There are no investment restrictions however, for solvency purposes only admissible assets considered Director: Appointment of local directors is not mandatory Note: (1) NPI refers to ‘Net Premium Income’ Domicile website – www.icb.gov.bs © 2014 KPMG, a Bahamas partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, (“KPMG International”) a Swiss entity. All rights reserved. 5

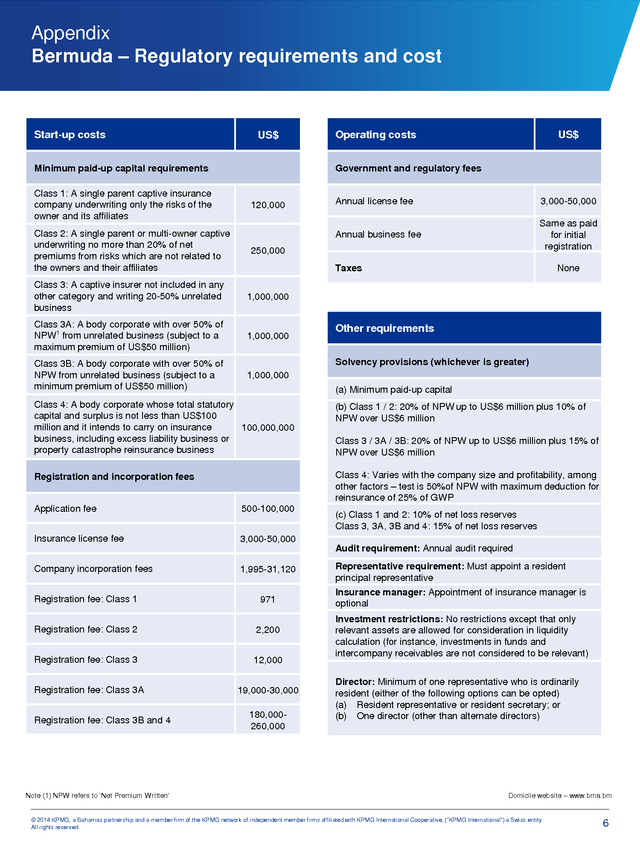

7) Appendix Bermuda – Regulatory requirements and cost Start-up costs US$ Minimum paid-up capital requirements Class 1: A single parent captive insurance company underwriting only the risks of the owner and its affiliates Class 2: A single parent or multi-owner captive underwriting no more than 20% of net premiums from risks which are not related to the owners and their affiliates Operating costs US$ Government and regulatory fees Annual license fee 3,000-50,000 Annual business fee 120,000 Same as paid for initial registration 250,000 Taxes Class 3: A captive insurer not included in any other category and writing 20-50% unrelated business 1,000,000 Class 3A: A body corporate with over 50% of NPW1 from unrelated business (subject to a maximum premium of US$50 million) 1,000,000 Class 3B: A body corporate with over 50% of NPW from unrelated business (subject to a minimum premium of US$50 million) None 1,000,000 Other requirements Solvency provisions (whichever is greater) (a) Minimum paid-up capital Class 4: A body corporate whose total statutory capital and surplus is not less than US$100 million and it intends to carry on insurance 100,000,000 business, including excess liability business or property catastrophe reinsurance business (b) Class 1 / 2: 20% of NPW up to US$6 million plus 10% of NPW over US$6 million Registration and incorporation fees Class 4: Varies with the company size and profitability, among other factors – test is 50%of NPW with maximum deduction for reinsurance of 25% of GWP Application fee 500-100,000 Insurance license fee Class 3 / 3A / 3B: 20% of NPW up to US$6 million plus 15% of NPW over US$6 million 3,000-50,000 (c) Class 1 and 2: 10% of net loss reserves Class 3, 3A, 3B and 4: 15% of net loss reserves Audit requirement: Annual audit required Company incorporation fees 1,995-31,120 Registration fee: Class 1 971 Registration fee: Class 2 2,200 Registration fee: Class 3 12,000 Registration fee: Class 3A Registration fee: Class 3B and 4 Note:(1) NPW refers to ‘Net Premium Written’ 19,000-30,000 180,000260,000 Representative requirement: Must appoint a resident principal representative Insurance manager: Appointment of insurance manager is optional Investment restrictions: No restrictions except that only relevant assets are allowed for consideration in liquidity calculation (for instance, investments in funds and intercompany receivables are not considered to be relevant) Director: Minimum of one representative who is ordinarily resident (either of the following options can be opted) (a) Resident representative or resident secretary; or (b) One director (other than alternate directors) Domicile website – www.bma.bm © 2014 KPMG, a Bahamas partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, (“KPMG International”) a Swiss entity. All rights reserved. 6

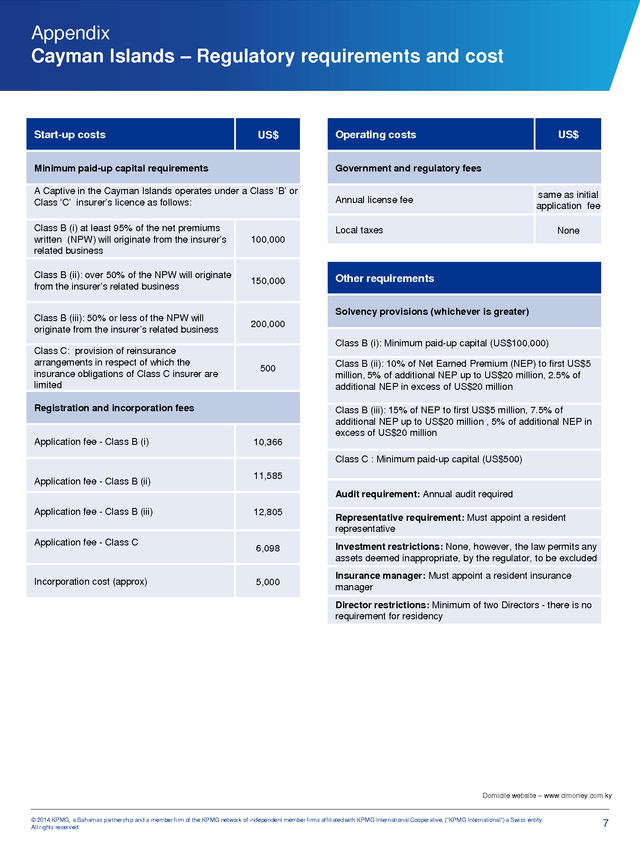

8) Appendix Cayman Islands – Regulatory requirements and cost Start-up costs US$ Operating costs Minimum paid-up capital requirements Government and regulatory fees A Captive in the Cayman Islands operates under a Class ‘B’ or Class ‘C’ insurer’s licence as follows: US$ Annual license fee Class B (i) at least 95% of the net premiums written (NPW) will originate from the insurer’s related business 100,000 Class B (ii): over 50% of the NPW will originate from the insurer’s related business 150,000 Class B (iii): 50% or less of the NPW will originate from the insurer’s related business same as initial application fee 200,000 Class C: provision of reinsurance arrangements in respect of which the insurance obligations of Class C insurer are limited Local taxes Other requirements Solvency provisions (whichever is greater) Class B (i): Minimum paid-up capital (US$100,000) 500 Registration and incorporation fees Application fee - Class B (i) None Class B (ii): 10% of Net Earned Premium (NEP) to first US$5 million, 5% of additional NEP up to US$20 million, 2.5% of additional NEP in excess of US$20 million Class B (iii): 15% of NEP to first US$5 million, 7.5% of additional NEP up to US$20 million , 5% of additional NEP in excess of US$20 million 10,366 Class C : Minimum paid-up capital (US$500) Application fee - Class B (ii) 11,585 Audit requirement: Annual audit required Application fee - Class B (iii) Application fee - Class C Incorporation cost (approx) 12,805 Representative requirement: Must appoint a resident representative 6,098 Investment restrictions: None, however, the law permits any assets deemed inappropriate, by the regulator, to be excluded 5,000 Insurance manager: Must appoint a resident insurance manager Director restrictions: Minimum of two Directors - there is no requirement for residency Domicile website – www.cimoney.com.ky © 2014 KPMG, a Bahamas partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, (“KPMG International”) a Swiss entity. All rights reserved. 7

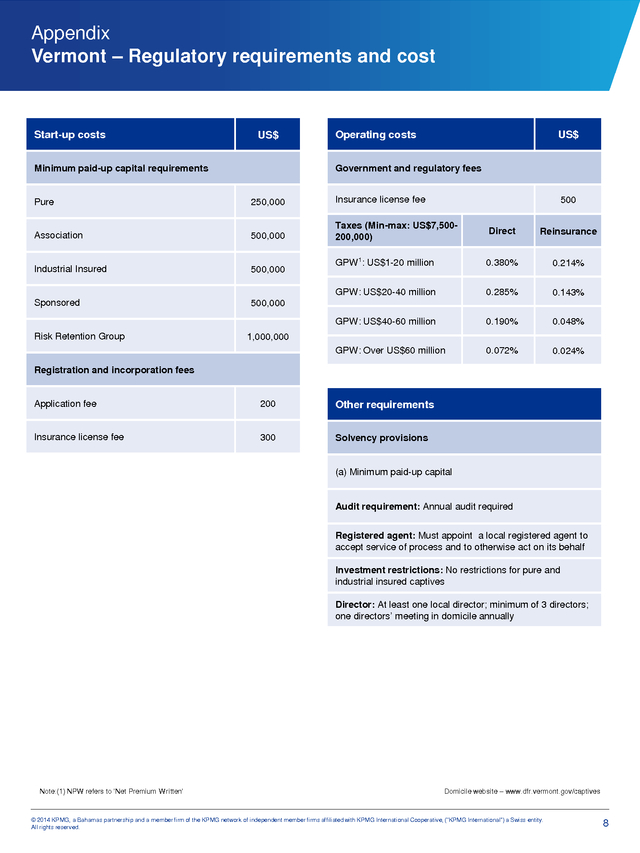

9) Appendix Vermont – Regulatory requirements and cost Start-up costs US$ Operating costs US$ Government and regulatory fees Minimum paid-up capital requirements Pure 250,000 Insurance license fee Association 500,000 Taxes (Min-max: US$7,500200,000) Direct Reinsurance Industrial Insured 500,000 GPW1: US$1-20 million 0.380% 0.214% GPW: US$20-40 million 0.285% 0.143% Sponsored 500,000 GPW: US$40-60 million 0.190% 0.048% GPW: Over US$60 million 0.072% 0.024% Risk Retention Group 500 1,000,000 Registration and incorporation fees Application fee 200 Other requirements Insurance license fee 300 Solvency provisions (a) Minimum paid-up capital Audit requirement: Annual audit required Registered agent: Must appoint a local registered agent to accept service of process and to otherwise act on its behalf Investment restrictions: No restrictions for pure and industrial insured captives Director: At least one local director; minimum of 3 directors; one directors’ meeting in domicile annually Note:(1) NPW refers to ‘Net Premium Written’ Domicile website – www.dfr.vermont.gov/captives © 2014 KPMG, a Bahamas partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, (“KPMG International”) a Swiss entity. All rights reserved. 8

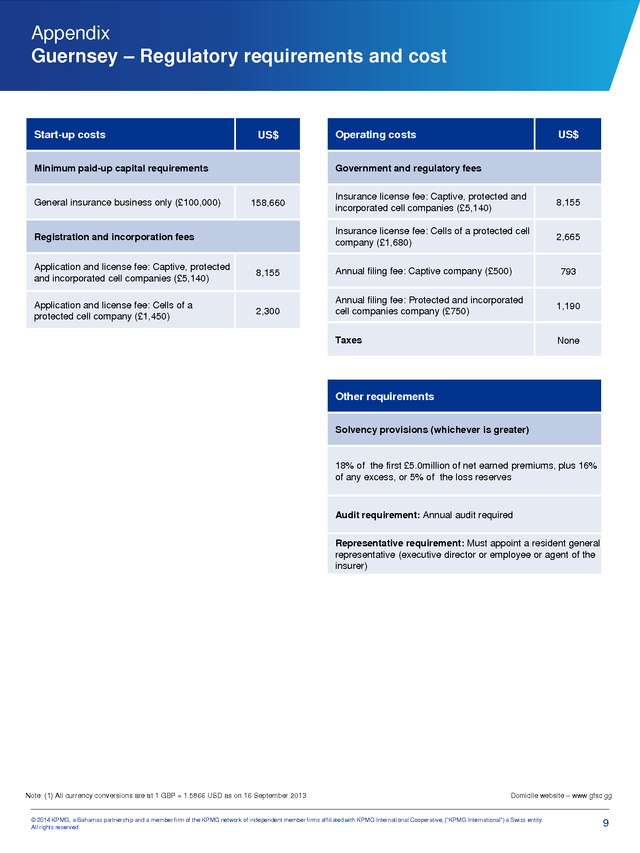

10) Appendix Guernsey – Regulatory requirements and cost Start-up costs US$ Minimum paid-up capital requirements General insurance business only (£100,000) Operating costs US$ Government and regulatory fees Registration and incorporation fees Insurance license fee: Captive, protected and incorporated cell companies (£5,140) 8,155 Insurance license fee: Cells of a protected cell company (£1,680) 158,660 2,665 Application and license fee: Captive, protected and incorporated cell companies (£5,140) 8,155 Annual filing fee: Captive company (£500) Application and license fee: Cells of a protected cell company (£1,450) 2,300 Annual filing fee: Protected and incorporated cell companies company (£750) 1,190 Taxes None 793 Other requirements Solvency provisions (whichever is greater) 18% of the first £5.0million of net earned premiums, plus 16% of any excess, or 5% of the loss reserves Audit requirement: Annual audit required Representative requirement: Must appoint a resident general representative (executive director or employee or agent of the insurer) Note: (1) All currency conversions are at 1 GBP = 1.5866 USD as on 16 September 2013 Domicile website – www.gfsc.gg © 2014 KPMG, a Bahamas partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, (“KPMG International”) a Swiss entity. All rights reserved. 9

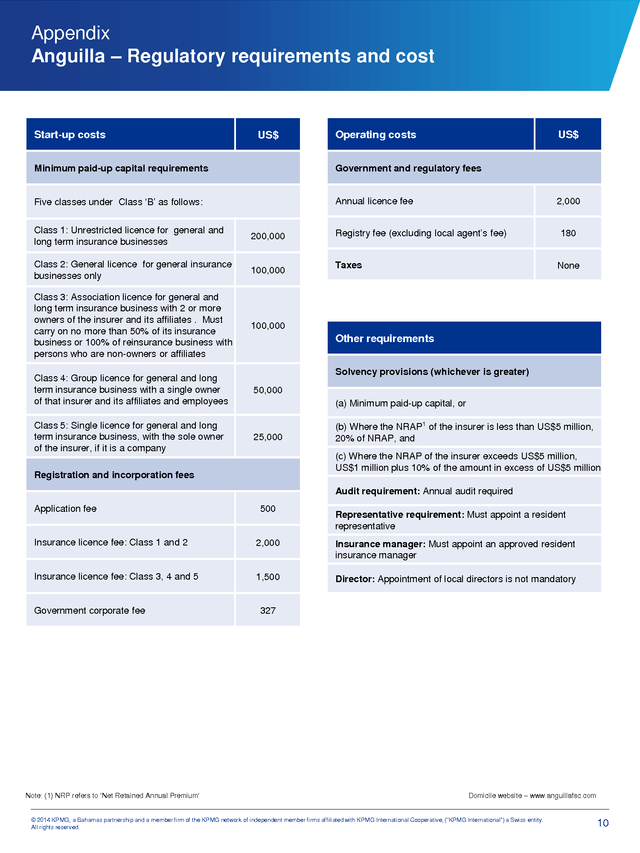

11) Appendix Anguilla – Regulatory requirements and cost Start-up costs US$ Operating costs US$ Minimum paid-up capital requirements Government and regulatory fees Five classes under Class ‘B’ as follows: Annual licence fee Class 1: Unrestricted licence for general and long term insurance businesses 200,000 Class 2: General licence for general insurance businesses only 100,000 Class 3: Association licence for general and long term insurance business with 2 or more owners of the insurer and its affiliates . Must carry on no more than 50% of its insurance business or 100% of reinsurance business with persons who are non-owners or affiliates 100,000 Class 4: Group licence for general and long term insurance business with a single owner of that insurer and its affiliates and employees 50,000 Class 5: Single licence for general and long term insurance business, with the sole owner of the insurer, if it is a company 25,000 2,000 Registry fee (excluding local agent’s fee) Taxes 180 None Other requirements Solvency provisions (whichever is greater) (a) Minimum paid-up capital, or (b) Where the NRAP1 of the insurer is less than US$5 million, 20% of NRAP, and (c) Where the NRAP of the insurer exceeds US$5 million, US$1 million plus 10% of the amount in excess of US$5 million Registration and incorporation fees Audit requirement: Annual audit required Application fee 500 Representative requirement: Must appoint a resident representative Insurance licence fee: Class 1 and 2 2,000 Insurance manager: Must appoint an approved resident insurance manager Insurance licence fee: Class 3, 4 and 5 1,500 Director: Appointment of local directors is not mandatory Government corporate fee Note: (1) NRP refers to ‘Net Retained Annual Premium’ 327 Domicile website – www.anguillafsc.com © 2014 KPMG, a Bahamas partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, (“KPMG International”) a Swiss entity. All rights reserved. 10

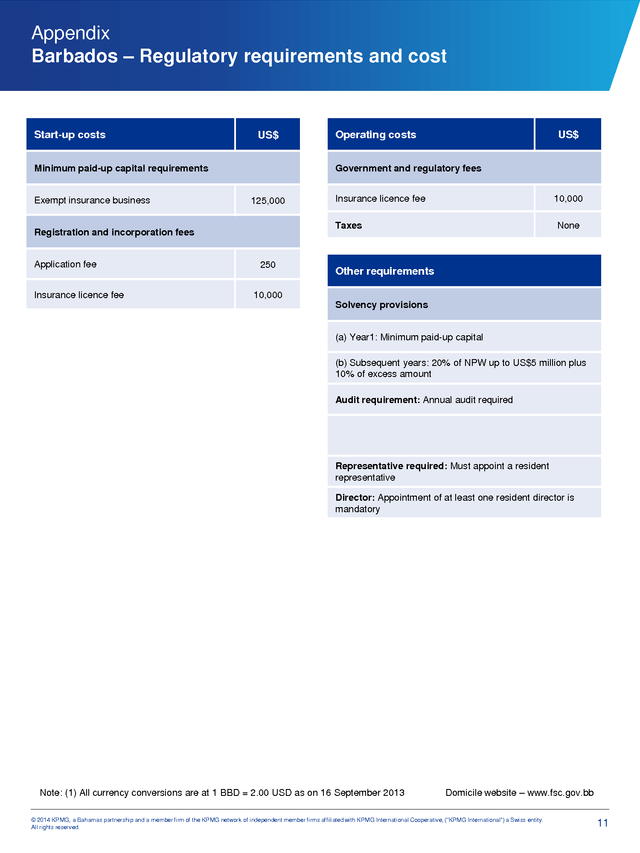

12) Appendix Barbados – Regulatory requirements and cost Start-up costs US$ Minimum paid-up capital requirements Exempt insurance business Insurance licence fee US$ Government and regulatory fees 125,000 Insurance licence fee 10,000 Taxes Registration and incorporation fees Application fee Operating costs 250 None Other requirements 10,000 Solvency provisions (a) Year1: Minimum paid-up capital (b) Subsequent years: 20% of NPW up to US$5 million plus 10% of excess amount Audit requirement: Annual audit required Representative required: Must appoint a resident representative Director: Appointment of at least one resident director is mandatory Note: (1) All currency conversions are at 1 BBD = 2.00 USD as on 16 September 2013 Domicile website – www.fsc.gov.bb © 2014 KPMG, a Bahamas partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, (“KPMG International”) a Swiss entity. All rights reserved. 11

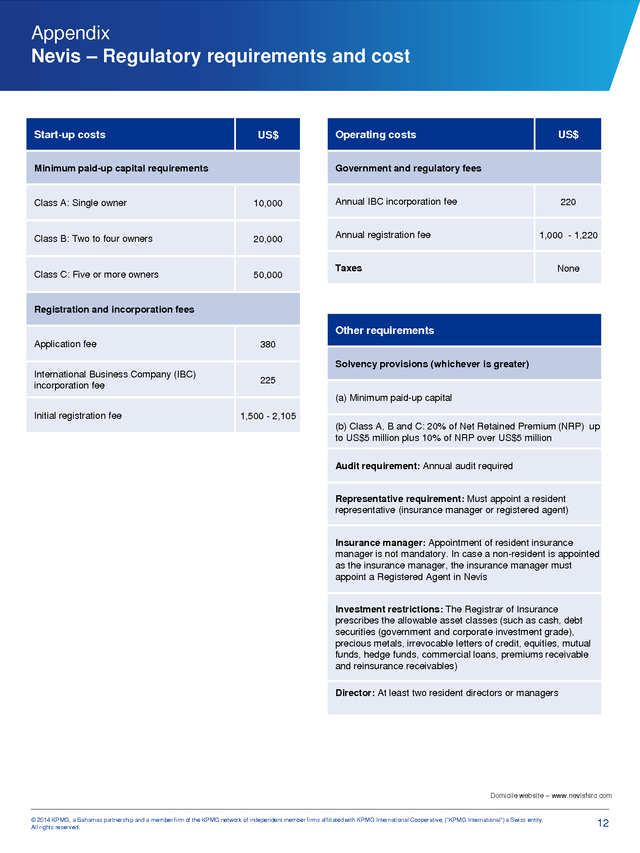

13) Appendix Nevis – Regulatory requirements and cost Start-up costs US$ Minimum paid-up capital requirements Operating costs US$ Government and regulatory fees Class A: Single owner 10,000 Annual IBC incorporation fee Class B: Two to four owners 20,000 Annual registration fee Class C: Five or more owners 50,000 220 1,000 - 1,220 Taxes None Registration and incorporation fees Other requirements Application fee 380 International Business Company (IBC) incorporation fee 225 Solvency provisions (whichever is greater) (a) Minimum paid-up capital Initial registration fee 1,500 - 2,105 (b) Class A, B and C: 20% of Net Retained Premium (NRP) up to US$5 million plus 10% of NRP over US$5 million Audit requirement: Annual audit required Representative requirement: Must appoint a resident representative (insurance manager or registered agent) Insurance manager: Appointment of resident insurance manager is not mandatory. In case a non-resident is appointed as the insurance manager, the insurance manager must appoint a Registered Agent in Nevis Investment restrictions: The Registrar of Insurance prescribes the allowable asset classes (such as cash, debt securities (government and corporate investment grade), precious metals, irrevocable letters of credit, equities, mutual funds, hedge funds, commercial loans, premiums receivable and reinsurance receivables) Director: At least two resident directors or managers Domicile website – www.nevisfsrc.com © 2014 KPMG, a Bahamas partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, (“KPMG International”) a Swiss entity. All rights reserved. 12

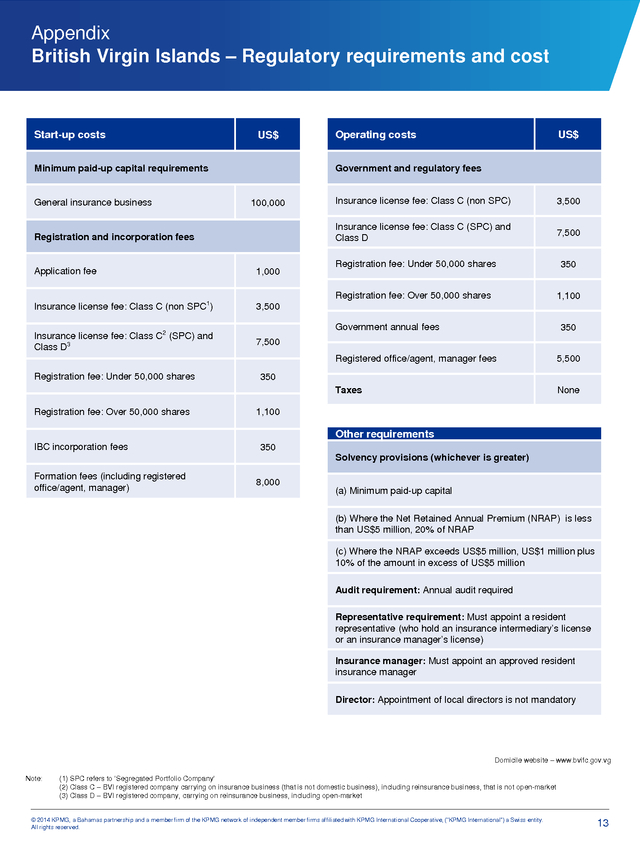

14) Appendix British Virgin Islands – Regulatory requirements and cost Start-up costs US$ Minimum paid-up capital requirements General insurance business Operating costs US$ Government and regulatory fees Registration and incorporation fees Insurance license fee: Class C (non SPC) 3,500 Insurance license fee: Class C (SPC) and Class D 100,000 7,500 1,000 Insurance license fee: Class C (non SPC1) 350 1,100 3,500 Insurance license fee: Class C2 (SPC) and Class D3 Registration fee: Under 50,000 shares Registration fee: Over 50,000 shares Application fee 7,500 Government annual fees 350 Registered office/agent, manager fees Taxes Registration fee: Under 50,000 shares Registration fee: Over 50,000 shares 5,500 None 350 1,100 Other requirements IBC incorporation fees 350 Solvency provisions (whichever is greater) Formation fees (including registered office/agent, manager) 8,000 (a) Minimum paid-up capital (b) Where the Net Retained Annual Premium (NRAP) is less than US$5 million, 20% of NRAP (c) Where the NRAP exceeds US$5 million, US$1 million plus 10% of the amount in excess of US$5 million Audit requirement: Annual audit required Representative requirement: Must appoint a resident representative (who hold an insurance intermediary’s license or an insurance manager’s license) Insurance manager: Must appoint an approved resident insurance manager Director: Appointment of local directors is not mandatory Domicile website – www.bvifc.gov.vg Note: (1) SPC refers to ‘Segregated Portfolio Company’ (2) Class C – BVI registered company carrying on insurance business (that is not domestic business), including reinsurance business, that is not open-market (3) Class D – BVI registered company, carrying on reinsurance business, including open-market © 2014 KPMG, a Bahamas partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, (“KPMG International”) a Swiss entity. All rights reserved. 13

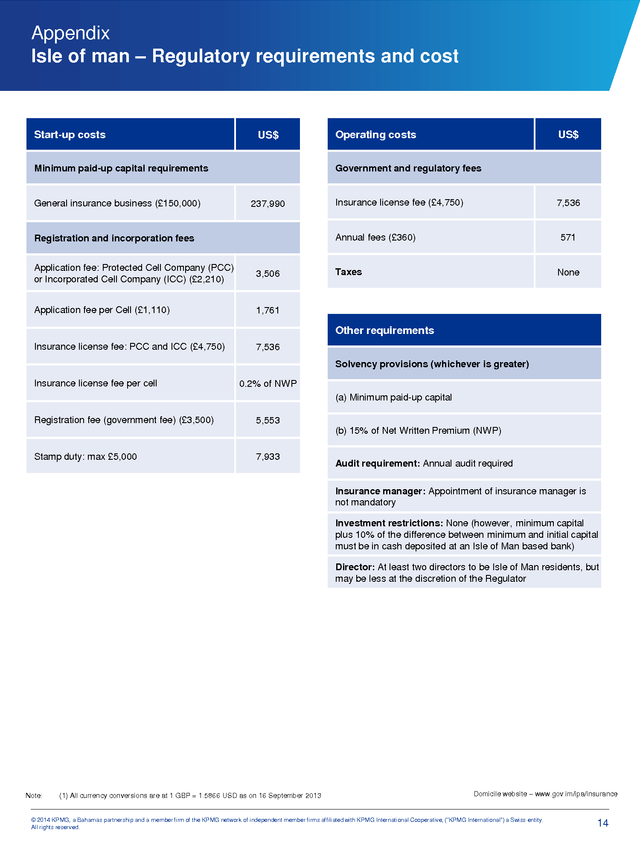

15) Appendix Isle of man – Regulatory requirements and cost Start-up costs US$ Minimum paid-up capital requirements General insurance business (£150,000) Operating costs US$ Government and regulatory fees 237,990 Insurance license fee (£4,750) 7,536 Annual fees (£360) Registration and incorporation fees Application fee: Protected Cell Company (PCC) or Incorporated Cell Company (ICC) (£2,210) 3,506 Application fee per Cell (£1,110) 1,761 Insurance license fee: PCC and ICC (£4,750) 571 7,536 Taxes None Other requirements Solvency provisions (whichever is greater) Insurance license fee per cell 0.2% of NWP (a) Minimum paid-up capital Registration fee (government fee) (£3,500) 5,553 (b) 15% of Net Written Premium (NWP) Stamp duty: max £5,000 7,933 Audit requirement: Annual audit required Insurance manager: Appointment of insurance manager is not mandatory Investment restrictions: None (however, minimum capital plus 10% of the difference between minimum and initial capital must be in cash deposited at an Isle of Man based bank) Director: At least two directors to be Isle of Man residents, but may be less at the discretion of the Regulator Note: (1) All currency conversions are at 1 GBP = 1.5866 USD as on 16 September 2013 Domicile website – www.gov.im/ipa/insurance © 2014 KPMG, a Bahamas partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, (“KPMG International”) a Swiss entity. All rights reserved. 14

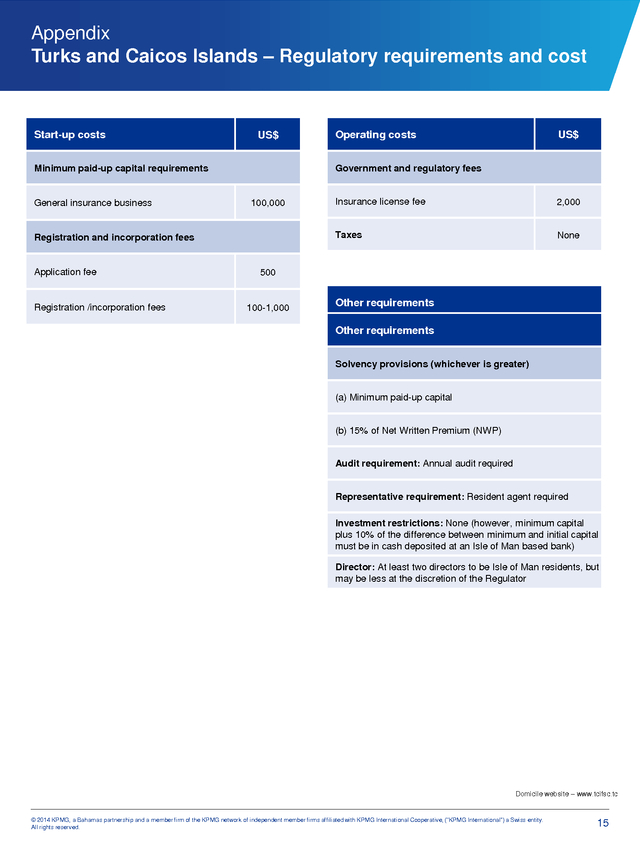

16) Appendix Turks and Caicos Islands – Regulatory requirements and cost Start-up costs US$ Minimum paid-up capital requirements General insurance business Registration /incorporation fees US$ Government and regulatory fees Insurance license fee 2,000 Taxes 100,000 Registration and incorporation fees Application fee Operating costs None 500 100-1,000 Other requirements Other requirements Solvency provisions (whichever is greater) (a) Where provisions Premium Income (API) is less than Solvency the Annual (whichever is greater) US$5 million, 20% of API (b) Minimum paid-up capitalUS$5 million, US$1 million plus (a) Where the API exceeds 10% of the excess amount (b) 15% of Net Written Premium (NWP) Audit requirement: Annual audit required Investment restrictions: No restrictions (however, only highly Audit requirement: Annual audit required liquid assets are considered for solvency assessment) Representative requirement: Resident agent required local Director: Minimum of two directors, none required to be Investment restrictions: None (however, minimum capital plus 10% of the difference between minimum and initial capital must be in cash deposited at an Isle of Man based bank) Director: At least two directors to be Isle of Man residents, but may be less at the discretion of the Regulator Domicile website – www.tcifsc.tc © 2014 KPMG, a Bahamas partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, (“KPMG International”) a Swiss entity. All rights reserved. 15

17) About the Regulator Insurance Commission of The Bahamas The Insurance Commission of The Bahamas is an independent authority responsible for licensing and regulating insurance companies operating in and from The Bahamas. The Insurance Commission of The Bahamas was established on July 2, 2009, under The Insurance Act, Chapter 347. The insurance sector is of fundamental economic and social importance both domestically and internationally. It is therefore important for the sector to be regulated in accordance with international standards and best practices, so as to ensure that both the domestic insurers and those insurers operating on an international level, but domiciled in The Bahamas, are appropriately supervised, in order to maintain efficient, fair, safe and stable insurance markets for the benefit and protection of policyholders. Having an independent regulatory agency is a fundamental requirement of international best practices embodied in the core principles of the International Association of Insurance Supervisors (IAIS). These core principles are the standards for international best practices for insurance supervision, and are used by the World Bank and the International Monetary Fund in their Financial Sector Assessment Programme (FSAP). Since July 2009 the Commission and the industry have made significant progress in developing the local regulatory and supervisory regime ,so that it is more closely aligned with international standards. The Commission is both the Prudential and Market Conduct regulator, and its purpose is to ensure a sound and stable insurance marketplace and consumer confidence in the insurance industry. The mandate of the Commission includes: •Administration of the Insurance Act and the External Insurance Act •Insurance market surveillance •Promoting and encouraging sound and prudent insurance management and business practices •Advising the Minister responsible for insurance matters •Compliance with FTRA and AML legislation. The Commission contributes to the overall safety and soundness of regulated financial institutions and regulates market conduct through a programme of supervision, regulations and public information. Policyholder protection is of paramount importance and significance . Contact The Insurance Commission of The Bahamas P.O. Box N 4844 Charlotte House, 3rd Floor Charlotte & Shirley Streets Nassau, N.P. The Bahamas Tel: +(242) 397-4100 Fax:+(242) 328-7010 www.icb.gov.bs © 2014 KPMG, a Bahamas partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, (“KPMG International”) a Swiss entity. All rights reserved. 16

18) Bahamas Financial Services Board About BFSB The Bahamas Financial Services Board (BFSB), launched in April 1998, represents an innovative commitment by the financial services industry and the Government of The Bahamas to promote a greater awareness of The Bahamas' strengths as an international financial centre. BFSB is a multidisciplinary body that embraces active contribution from individuals within government, banking, trust and investment advisory services, insurance and investment fund administration as well as interested legal, accounting and management professionals. BFSB represents and promotes the development of all sectors of the industry, including: banking, private banking and trust services, investment funds, capital markets, investment advisory services, accounting and legal services, insurance, and corporate and shipping registry. In addition to its coordinated programs to increase confidence and expand knowledge of The Bahamas among international businesses and investors, the private sector-led BFSB will continue to consult with government to develop new initiatives to meet the rapidly changing demands of international financial markets The Bahamas' long-standing tradition of democracy (one of the oldest in the hemisphere), and independent stability since 1973, have been significant attributes in the development of financial services sector. BFSB is guided by the same principles. It does not supplant existing financial services associations that continue to serve individual professional groups within the industry as they have in the past. Rather, BFSB complements them, drawing much of its strength from close intra-industry participation and collaboration. BFSB’s costs, including those of an experienced, active, full-time executive director, are shared by government and the private sector through membership fees. Board members are elected to two-year terms by voting member representatives. Contact Bahamas Financial Services Board P.O. Box N 1764 Montague Sterling Centre, 2nd Floor East Bay Street Nassau, N.P. The Bahamas Tel: +(242) 393-7001 Fax:+(242) 393-7712 www.bfsb-bahamas.com © 2014 KPMG, a Bahamas partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, (“KPMG International”) a Swiss entity. All rights reserved. 17

19) KPMG A global network KPMG is a global network of professional services firms of KPMG International Cooperative, a Swiss entity. Our member firms provide audit, tax and advisory services through industry-focused, talented professionals who deliver value for the benefit of their clients and communities. With more than 152,000 people worldwide, KPMG member firms provide audit, tax and advisory services in 156 countries working closely with our clients, helping them to mitigate risks and grasp opportunities. KPMG in The Bahamas KPMG in The Bahamas is one of the largest accounting and advisory service firms in the country, operating from offices in Nassau and Freeport. The firm has a total staff of 81 led by 5 partners and 4 principals. KPMG in The Bahamas provides a wide range of professional services to businesses around the world. We provide our clients with focused industry knowledge, multidisciplinary teams and substantive experience in audit, tax and advisory. Contact KPMG P.O. Box N 123 Montague Sterling Centre East Bay Street Nassau, N.P. The Bahamas Tel: +(242) 393-2007 Fax:+(242) 393-1772 www.kpmg.com © 2014 KPMG, a Bahamas partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, (“KPMG International”) a Swiss entity. All rights reserved. 18

20) The information contained herein is of general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavour to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation. © 2014 KPMG, a Bahamian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International Cooperative (“KPMG International”).