1) Q1 2016 Catastrophe

Bond & ILS Market Report

Another record first-quarter

ARTEMIS

Focused on insurance-linked securities (ILS), catastrophe bonds,

alternative reinsurance capital and related risk transfer markets.

CO- EDITOR:

www.artemis.bm

�

2) B E R M U D A

THE WORLD’S

CONVERGENCE

C A P I T A L

Visionary industry leaders. Sophisticated infrastructure.

Speed to market. A hub of talent, experience and innovation.

Bermuda is a blue-chip financial centre built on pioneering ideas

and globally respected regulation. We attract the world’s leading

underwriters and asset managers—a natural nexus for convergence

of reinsurance and financial markets.

With more than 70 percent of global insurance-linked securities listed,

Bermuda is a centre of excellence for the creation, support and listing of

cat bonds, collateralized reinsurance, derivative instruments and other

unique vehicles. Does your capital belong here?

Learn more at bda.bm

Connecting Business

Maxwell Roberts Building, 6th Floor

1 Church Street

Hamilton HM 11

Bermuda

+ 1 4 41 292 0 632

info@bda.bm

w w w.bda.bm

�

3) INTRO

This report reviews the catastrophe bond and insurance-linked

securities (ILS) market at the end of the first-quarter of 2016, looking

at new risk capital issued and the composition of transactions

completed during the quarter.

For the first time in its history the catastrophe bond and ILS market has

ended a quarter with more than $26 billion of outstanding market capacity,

driven by a record-breaking start to the year that saw $2.215 billion of new

risk capital issued from ten transactions, lifting the outstanding market to

$26.516 billion at the end of March 2016.

The first-quarter is often a busy period for the sector as renewal deals come

to market. An impressive $800 million of deals were issued during January, the

second strongest January issuance volume ever recorded by Artemis, but more

than $1.4 billion of new deals in February and March helped the market achieve

outright growth once again.

Despite a substantial lack of privately placed deal issuance (or disclosure) in Q1

2016, particularly when compared to a year earlier when almost half of new

deals issued were considered private, sponsor and investor appetite clearly

remained strong during the quarter keeping the market on its impressive

growth path.

Artemis is the leading, freely accessible source of timely, relevant and

authoritative news, analysis, insight and data on the insurance-linked

securities, catastrophe bond, alternative reinsurance capital and related risk

transfer markets. The Artemis Deal Directory is the leading, freely available

source of information, data and analysis on issued catastrophe bond and

insurance-linked securitization transactions.

�

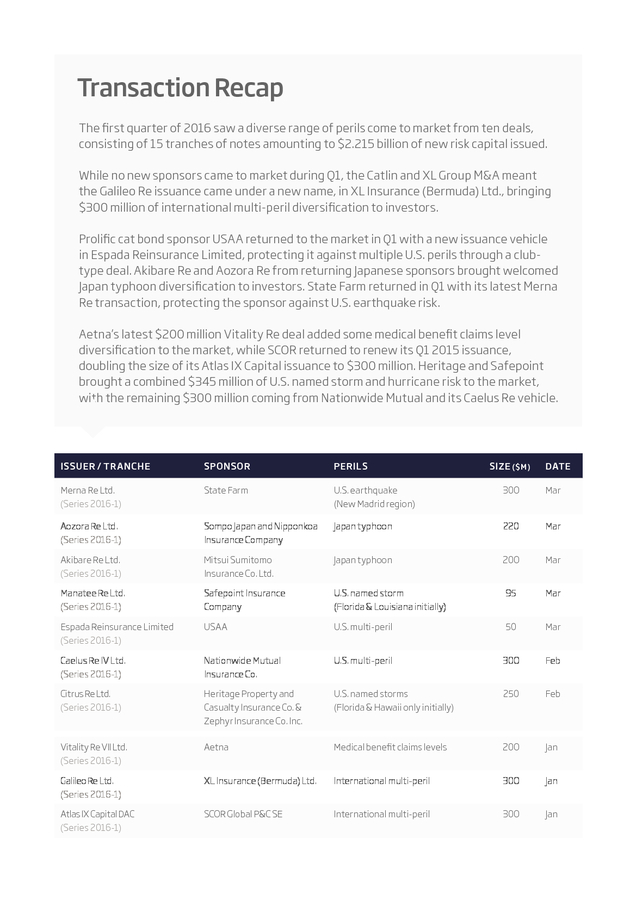

4) Transaction Recap

The first quarter of 2016 saw a diverse range of perils come to market from ten deals,

consisting of 15 tranches of notes amounting to $2.215 billion of new risk capital issued.

While no new sponsors came to market during Q1, the Catlin and XL Group M&A meant

the Galileo Re issuance came under a new name, in XL Insurance (Bermuda) Ltd., bringing

$300 million of international multi-peril diversification to investors.

Prolific cat bond sponsor USAA returned to the market in Q1 with a new issuance vehicle

in Espada Reinsurance Limited, protecting it against multiple U.S. perils through a clubtype deal. Akibare Re and Aozora Re from returning Japanese sponsors brought welcomed

Japan typhoon diversification to investors. State Farm returned in Q1 with its latest Merna

Re transaction, protecting the sponsor against U.S. earthquake risk.

Aetna’s latest $200 million Vitality Re deal added some medical benefit claims level

diversification to the market, while SCOR returned to renew its Q1 2015 issuance,

doubling the size of its Atlas IX Capital issuance to $300 million. Heritage and Safepoint

brought a combined $345 million of U.S. named storm and hurricane risk to the market,

with the remaining $300 million coming from Nationwide Mutual and its Caelus Re vehicle.

ISSUER / TRANCHE

SPONSOR

PERILS

SIZE ($M)

DATE

Merna Re Ltd.

(Series 2016-1)

State Farm

U.S. earthquake

(New Madrid region)

300

Mar

Aozora Re Ltd.

(Series 2016-1)

Sompo Japan and Nipponkoa

Insurance Company

Japan typhoon

220

Mar

Akibare Re Ltd.

(Series 2016-1)

Mitsui Sumitomo

Insurance Co. Ltd.

Japan typhoon

200

Mar

Manatee Re Ltd.

(Series 2016-1)

Safepoint Insurance

Company

U.S. named storm

(Florida & Louisiana initially)

95

Mar

Espada Reinsurance Limited

(Series 2016-1)

USAA

U.S. multi-peril

50

Mar

Caelus Re IV Ltd.

(Series 2016-1)

Nationwide Mutual

Insurance Co.

U.S. multi-peril

300

Feb

Citrus Re Ltd.

(Series 2016-1)

Heritage Property and

Casualty Insurance Co. &

Zephyr Insurance Co. Inc.

U.S. named storms

(Florida & Hawaii only initially)

250

Feb

Vitality Re VII Ltd.

(Series 2016-1)

Aetna

Medical benefit claims levels

200

Jan

Galileo Re Ltd.

(Series 2016-1)

XL Insurance (Bermuda) Ltd.

International multi-peril

300

Jan

Atlas IX Capital DAC

(Series 2016-1)

SCOR Global P&C SE

International multi-peril

300

Jan

�

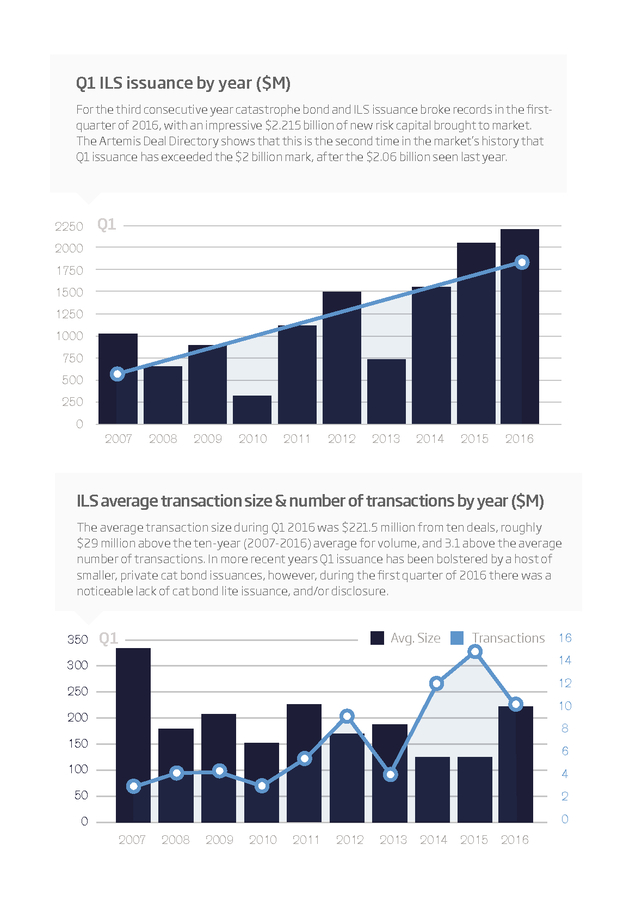

5) Q1 ILS issuance by year ($M)

For the third consecutive year catastrophe bond and ILS issuance broke records in the firstquarter of 2016, with an impressive $2.215 billion of new risk capital brought to market.

The Artemis Deal Directory shows that this is the second time in the market’s history that

Q1 issuance has exceeded the $2 billion mark, after the $2.06 billion seen last year.

2250

Q1

2000

1750

1500

1250

1000

750

500

250

0

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

ILS average transaction size & number of transactions by year ($M)

The average transaction size during Q1 2016 was $221.5 million from ten deals, roughly

$29 million above the ten-year (2007-2016) average for volume, and 3.1 above the average

number of transactions. In more recent years Q1 issuance has been bolstered by a host of

smaller, private cat bond issuances, however, during the first quarter of 2016 there was a

noticeable lack of cat bond lite issuance, and/or disclosure.

350

Avg. Size

Q1

Transactions 16

14

300

12

250

10

200

8

150

6

100

4

50

2

0

0

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

�

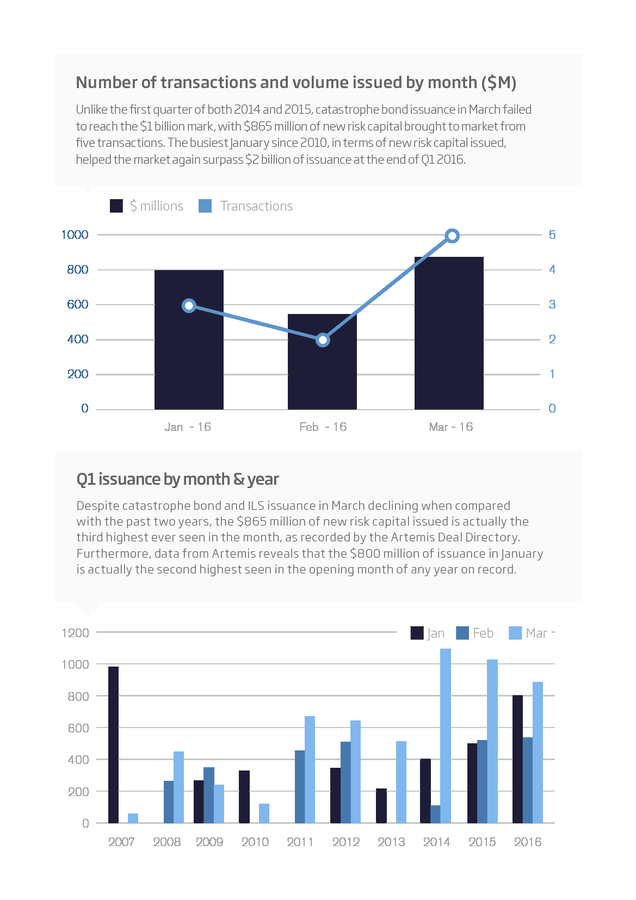

6) Number of transactions and volume issued by month ($M)

Unlike the first quarter of both 2014 and 2015, catastrophe bond issuance in March failed

to reach the $1 billion mark, with $865 million of new risk capital brought to market from

five transactions. The busiest January since 2010, in terms of new risk capital issued,

helped the market again surpass $2 billion of issuance at the end of Q1 2016.

$ millions

Transactions

1000

5

800

4

600

3

400

2

200

1

0

0

Jan - 16

Feb - 16

Mar - 16

Q1 issuance by month & year

Despite catastrophe bond and ILS issuance in March declining when compared

with the past two years, the $865 million of new risk capital issued is actually the

third highest ever seen in the month, as recorded by the Artemis Deal Directory.

Furthermore, data from Artemis reveals that the $800 million of issuance in January

is actually the second highest seen in the opening month of any year on record.

Jan

1200

Feb

2014

2015

Mar

1000

800

600

400

200

0

2007

2008

2009

2010

2011

2012

2013

2016

�

7) �

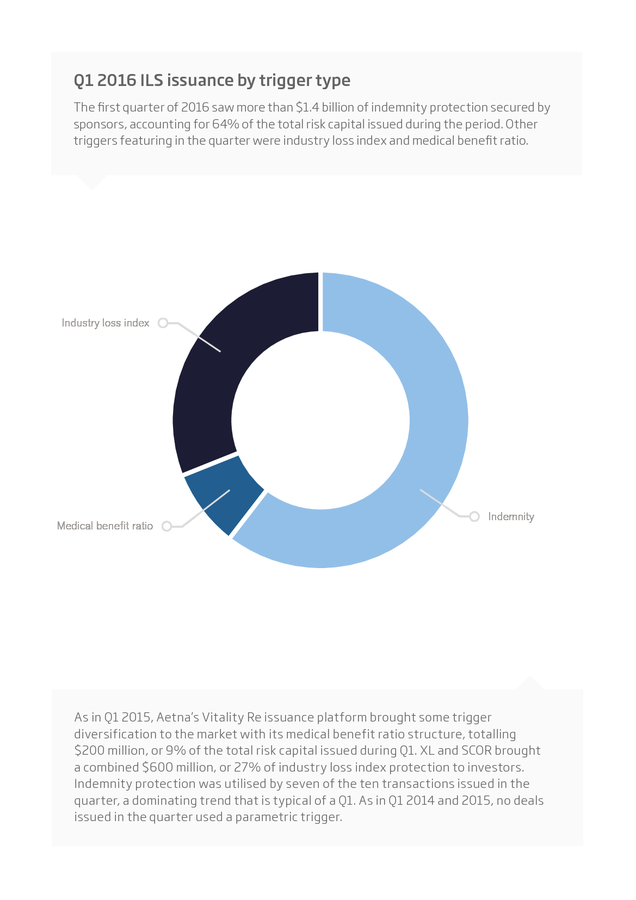

8) Q1 2016 ILS issuance by trigger type

The first quarter of 2016 saw more than $1.4 billion of indemnity protection secured by

sponsors, accounting for 64% of the total risk capital issued during the period. Other

triggers featuring in the quarter were industry loss index and medical benefit ratio.

Industry loss index

Medical benefit ratio

Indemnity

As in Q1 2015, Aetna’s Vitality Re issuance platform brought some trigger

diversification to the market with its medical benefit ratio structure, totalling

$200 million, or 9% of the total risk capital issued during Q1. XL and SCOR brought

a combined $600 million, or 27% of industry loss index protection to investors.

Indemnity protection was utilised by seven of the ten transactions issued in the

quarter, a dominating trend that is typical of a Q1. As in Q1 2014 and 2015, no deals

issued in the quarter used a parametric trigger.

�

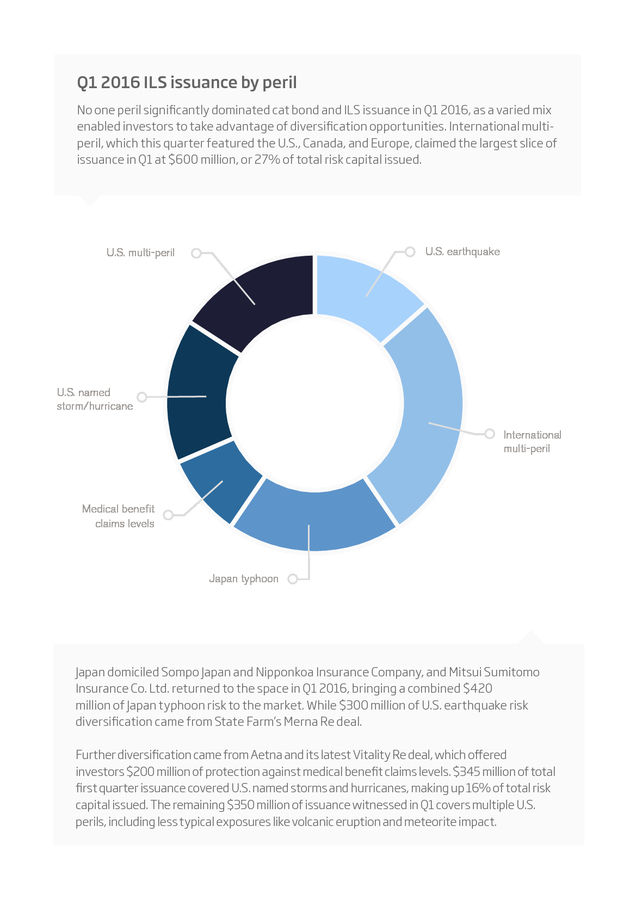

9) Q1 2016 ILS issuance by peril

No one peril significantly dominated cat bond and ILS issuance in Q1 2016, as a varied mix

enabled investors to take advantage of diversification opportunities. International multiperil, which this quarter featured the U.S., Canada, and Europe, claimed the largest slice of

issuance in Q1 at $600 million, or 27% of total risk capital issued.

U.S. earthquake

U.S. multi-peril

U.S. named

storm/hurricane

International

multi-peril

Medical benefit

claims levels

Japan typhoon

Japan domiciled Sompo Japan and Nipponkoa Insurance Company, and Mitsui Sumitomo

Insurance Co. Ltd. returned to the space in Q1 2016, bringing a combined $420

million of Japan typhoon risk to the market. While $300 million of U.S. earthquake risk

diversification came from State Farm’s Merna Re deal.

Further diversification came from Aetna and its latest Vitality Re deal, which offered

investors $200 million of protection against medical benefit claims levels. $345 million of total

first quarter issuance covered U.S. named storms and hurricanes, making up 16% of total risk

capital issued. The remaining $350 million of issuance witnessed in Q1 covers multiple U.S.

perils, including less typical exposures like volcanic eruption and meteorite impact.

�

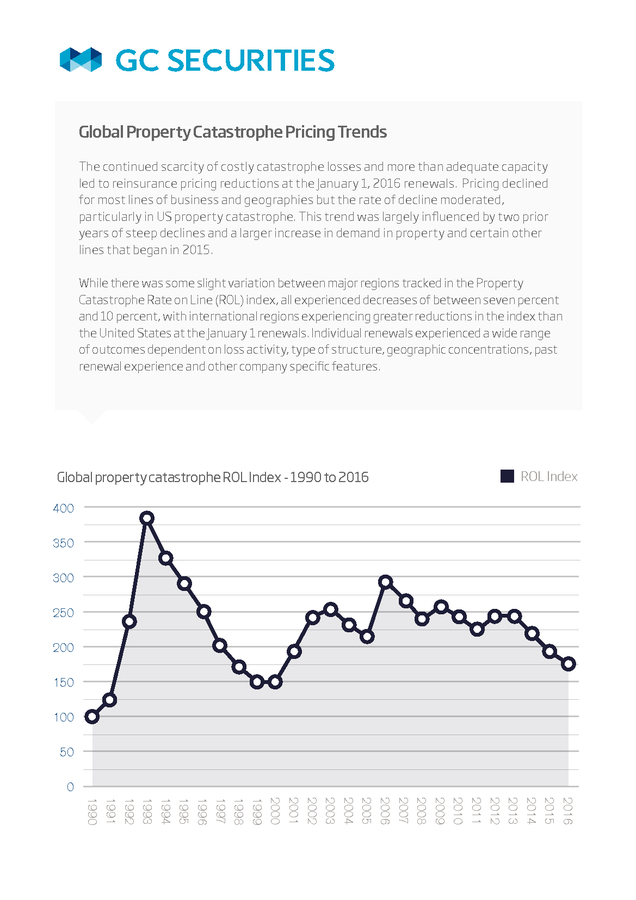

10) Global Property Catastrophe Pricing Trends

The continued scarcity of costly catastrophe losses and more than adequate capacity

led to reinsurance pricing reductions at the January 1, 2016 renewals. Pricing declined

for most lines of business and geographies but the rate of decline moderated,

particularly in US property catastrophe. This trend was largely influenced by two prior

years of steep declines and a larger increase in demand in property and certain other

lines that began in 2015.

While there was some slight variation between major regions tracked in the Property

Catastrophe Rate on Line (ROL) index, all experienced decreases of between seven percent

and 10 percent, with international regions experiencing greater reductions in the index than

the United States at the January 1 renewals. Individual renewals experienced a wide range

of outcomes dependent on loss activity, type of structure, geographic concentrations, past

renewal experience and other company specific features.

ROL Index

Global property catastrophe ROL Index - 1990 to 2016

400

350

300

250

200

150

100

50

0

2016

2015

2014

2013

2012

2011

2010

2009

2008

2007

2006

2005

2004

2003

2002

2001

2000

1999

1998

1997

1996

1995

1994

1993

1992

1991

1990

�

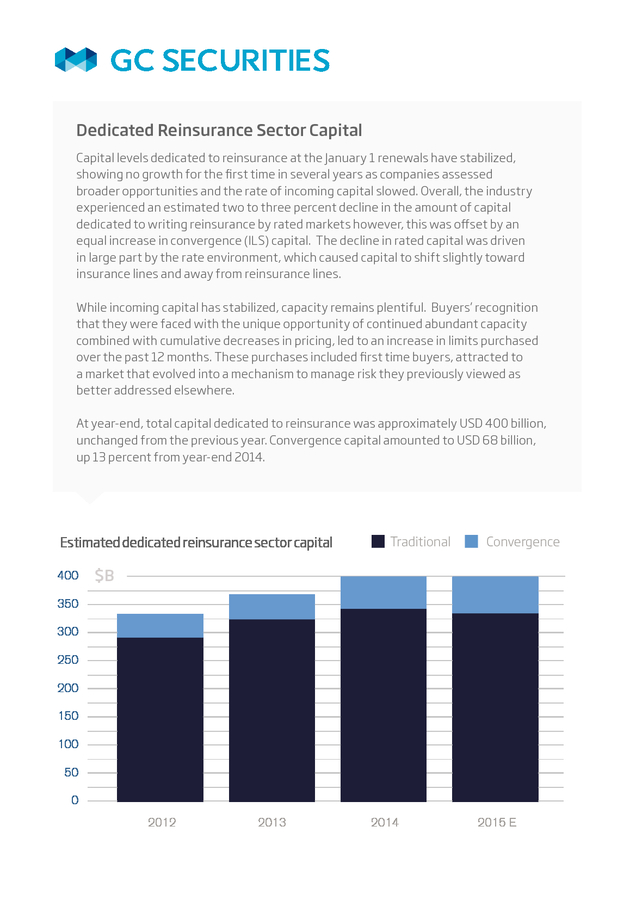

11) Dedicated Reinsurance Sector Capital

Capital levels dedicated to reinsurance at the January 1 renewals have stabilized,

showing no growth for the first time in several years as companies assessed

broader opportunities and the rate of incoming capital slowed. Overall, the industry

experienced an estimated two to three percent decline in the amount of capital

dedicated to writing reinsurance by rated markets however, this was offset by an

equal increase in convergence (ILS) capital. The decline in rated capital was driven

in large part by the rate environment, which caused capital to shift slightly toward

insurance lines and away from reinsurance lines.

While incoming capital has stabilized, capacity remains plentiful. Buyers’ recognition

that they were faced with the unique opportunity of continued abundant capacity

75%

70%

combined with cumulative decreases in pricing, led to an increase in limits purchased

over the past 12 months. These purchases included first time buyers, attracted to

a market that evolved into a mechanism to manage risk they previously viewed as

better addressed elsewhere.

At year-end, total capital dedicated to reinsurance was approximately USD 400 billion,

unchanged from the previous year. Convergence capital amounted to USD 68 billion,

up 13 percent from year-end 2014.

Estimated dedicated reinsurance sector capital

400

Traditional

Convergence

$B

350

300

250

200

150

100

50

0

2012

2013

2014

2015 E

�

12) 2016 Outlook

As the pricing environment showed signs of stabilization across both the

insurance-linked securities (ILS) and traditional markets, accessing multi-year

capacity at pre-agreed static rates is a focus for many cedents.

A significant and growing number of property programs were placed at least partially

on a multi-year basis at January 1 and notably, multi-year options are beginning to

emerge in some casualty sectors, where they have not been available in the past.

The capital markets are also in a strong position to provide multi-year capacity, and

2016 is expected to bring new opportunities in the ILS space for public sector entities,

corporates, insurers and reinsurers.

GC Securities, is a division of MMC Securities Corp., member FINRA/NFA/SIPC, main office: 1166 Avenue of the

Americas, New York, NY 10036, phone: 212.345.5000. MMC Securities Corp. and Guy Carpenter & Company, LLC are

affiliates and wholly owned by Marsh & McLennan Companies.

�

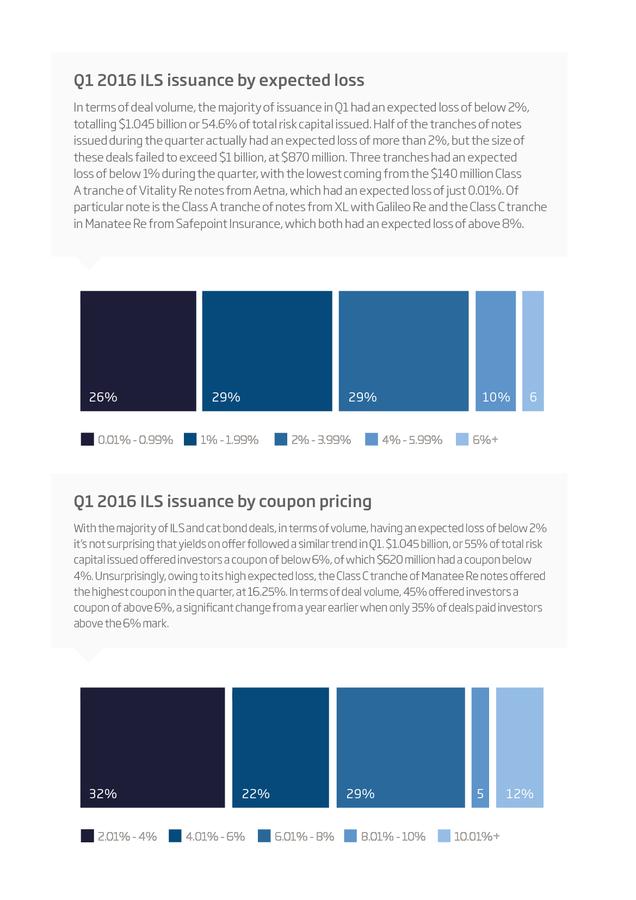

13) Q1 2016 ILS issuance by expected loss

In terms of deal volume, the majority of issuance in Q1 had an expected loss of below 2%,

totalling $1.045 billion or 54.6% of total risk capital issued. Half of the tranches of notes

issued during the quarter actually had an expected loss of more than 2%, but the size of

these deals failed to exceed $1 billion, at $870 million. Three tranches had an expected

loss of below 1% during the quarter, with the lowest coming from the $140 million Class

A tranche of Vitality Re notes from Aetna, which had an expected loss of just 0.01%. Of

particular note is the Class A tranche of notes from XL with Galileo Re and the Class C tranche

in Manatee Re from Safepoint Insurance, which both had an expected loss of above 8%.

v

v

26%

0.01% - 0.99%

29%

29%

1% - 1.99%

2% - 3.99%

10%

4% - 5.99%

6

6%+

Q1 2016 ILS issuance by coupon pricing

With the majority of ILS and cat bond deals, in terms of volume, having an expected loss of below 2%

it’s not surprising that yields on offer followed a similar trend in Q1. $1.045 billion, or 55% of total risk

capital issued offered investors a coupon of below 6%, of which $620 million had a coupon below

4%. Unsurprisingly, owing to its high expected loss, the Class C tranche of Manatee Re notes offered

the highest coupon in the quarter, at 16.25%. In terms of deal volume, 45% offered investors a

coupon of above 6%, a significant change from a year earlier when only 35% of deals paid investors

above the 6% mark.

v

v

32%

2.01% - 4%

22%

4.01% - 6%

29%

6.01% - 8%

8.01% - 10%

5

10.01%+

12%

�

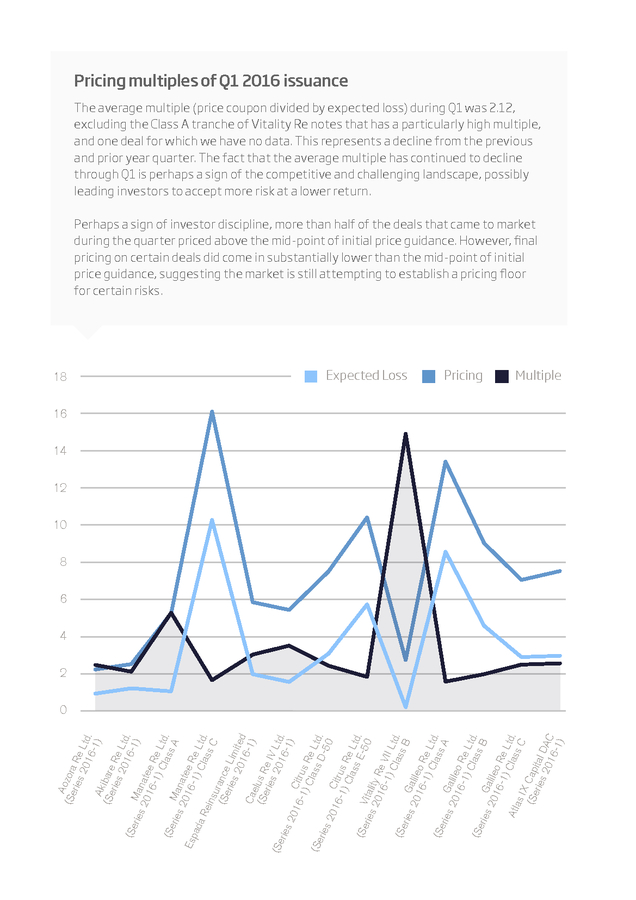

14) Pricing multiples of Q1 2016 issuance

The average multiple (price coupon divided by expected loss) during Q1 was 2.12,

excluding the Class A tranche of Vitality Re notes that has a particularly high multiple,

and one deal for which we have no data. This represents a decline from the previous

and prior year quarter. The fact that the average multiple has continued to decline

through Q1 is perhaps a sign of the competitive and challenging landscape, possibly

leading investors to accept more risk at a lower return.

Perhaps a sign of investor discipline, more than half of the deals that came to market

during the quarter priced above the mid-point of initial price guidance. However, final

pricing on certain deals did come in substantially lower than the mid-point of initial

price guidance, suggesting the market is still attempting to establish a pricing floor

for certain risks.

18

Expected Loss

Pricing

Multiple

16

14

12

10

8

6

4

2

A

(Se ozora

ries Re

20 Ltd

16 .

-1)

Ak

iba

(Se

re R

ries

20 e Ltd

16 .

(Se

-1)

ries Man

20 atee

16

Re

-1)

Cla Ltd.

(Se

ss

A

ries Man

20 atee

16

Esp

-1) Re L

ada

Cla td.

Re

ss

ins

C

ura

nce

(Se

ries Lim

20 ited

16

-1)

Ca

elu

(Se s R

ries e IV

(Se

20 Ltd

16 .

ries

-1)

20

16 Citru

-1)

sR

Cla e L

(Se

ss

D -5 td.

ries

0

20

16 Citru

-1)

s

Cla Re L

ss

E-5 td.

(Se

0

ries Vitali

20 ty R

16 e V

-1)

II L

Cla td.

(Se

ss

B

ries

G

20 alileo

16

-1) Re L

Cla td.

(Se

ss

A

ries

Ga

20 lileo

16

Re

-1)

Cla Ltd.

(Se

ss

B

ries

Ga

20 lileo

16

-1) Re L

Cla td.

Atla

ss

s IX

C

Ca

(Se

pita

ries

lD

20 AC

16

-1)

0

�

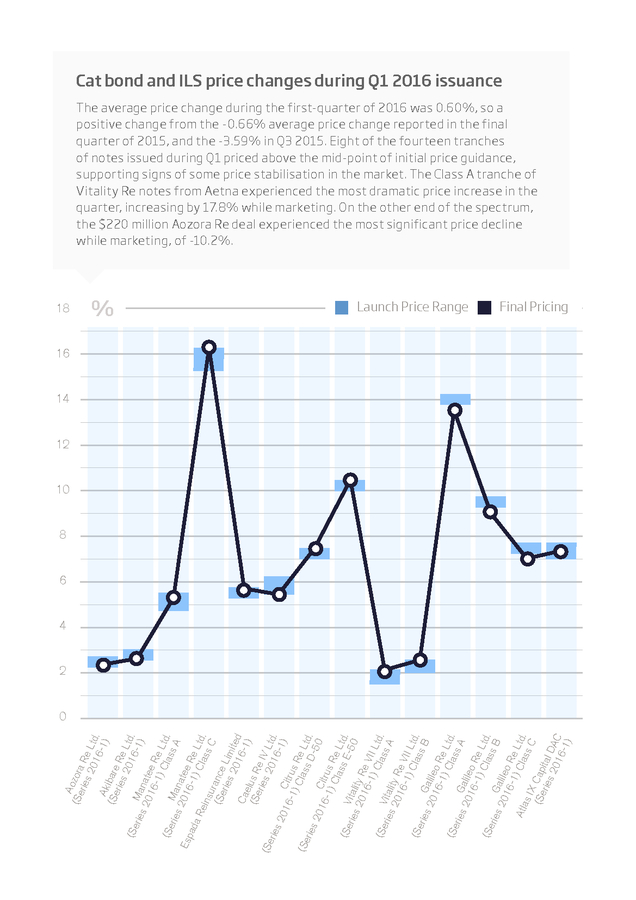

15) Cat bond and ILS price changes during Q1 2016 issuance

The average price change during the first-quarter of 2016 was 0.60%, so a

positive change from the -0.66% average price change reported in the final

quarter of 2015, and the -3.59% in Q3 2015. Eight of the fourteen tranches

of notes issued during Q1 priced above the mid-point of initial price guidance,

supporting signs of some price stabilisation in the market. The Class A tranche of

Vitality Re notes from Aetna experienced the most dramatic price increase in the

quarter, increasing by 17.8% while marketing. On the other end of the spectrum,

the $220 million Aozora Re deal experienced the most significant price decline

while marketing, of -10.2%.

18

%

Launch Price Range

Final Pricing

16

14

12

10

8

6

4

2

A

(Se ozora

ries Re

20 Ltd

16 .

-1)

Ak

(Se ibare

ries Re

20 Ltd

(Se

16 .

-1)

ries Man

20 atee

16

Re

-1)

Cla Ltd.

(Se

ss

ries Man

A

20 atee

Esp

16

Re

ada

-1)

Ltd

Cla

Re

ins

ss .

u

C

(Se rance

ries Lim

20 ited

16

Ca

-1)

e

(Se lus R

ries e IV

(Se

20 Ltd

ries

16 .

-1)

20

16 Citru

-1)

sR

Cla e L

(Se

ss

ries

D -5 td.

20

0

16 Citru

-1)

sR

Cla e L

ss

(Se

E-5 td.

ries Vitali

0

20 ty R

16 e V

-1)

II L

Cla td.

(Se

ss

ries Vitali

A

20 ty R

16 e V

-1)

II L

Cla td.

(Se

ss

ries

G

B

20 alileo

16

-1) Re L

Cla td.

(Se

ss

ries

G

A

20 alileo

16

Re

-1)

Cla Ltd.

(Se

ss

ries

B

G

20 alileo

16

Re

-1)

Ltd

Cla

Atla

ss .

s IX

C

(Se Cap

ries ital

20 DAC

16

-1)

0

�

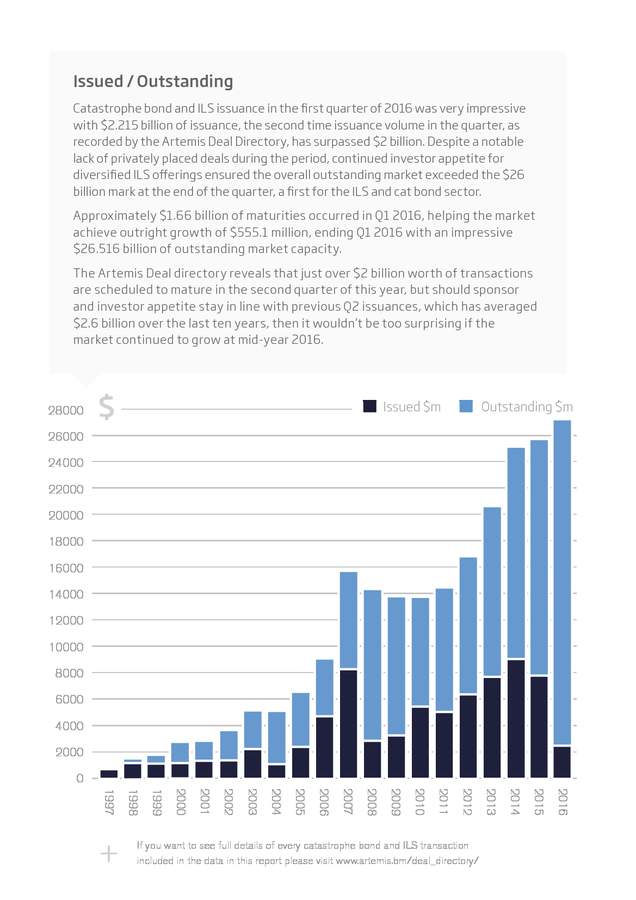

16) Issued / Outstanding

Catastrophe bond and ILS issuance in the first quarter of 2016 was very impressive

with $2.215 billion of issuance, the second time issuance volume in the quarter, as

recorded by the Artemis Deal Directory, has surpassed $2 billion. Despite a notable

lack of privately placed deals during the period, continued investor appetite for

diversified ILS offerings ensured the overall outstanding market exceeded the $26

billion mark at the end of the quarter, a first for the ILS and cat bond sector.

Approximately $1.66 billion of maturities occurred in Q1 2016, helping the market

achieve outright growth of $555.1 million, ending Q1 2016 with an impressive

$26.516 billion of outstanding market capacity.

The Artemis Deal directory reveals that just over $2 billion worth of transactions

are scheduled to mature in the second quarter of this year, but should sponsor

and investor appetite stay in line with previous Q2 issuances, which has averaged

$2.6 billion over the last ten years, then it wouldn’t be too surprising if the

market continued to grow at mid-year 2016.

28000

$

Issued $m

Outstanding $m

26000

24000

22000

20000

18000

16000

14000

12000

10000

8000

6000

4000

2000

0

2016

2015

2014

If you want to see full details of every catastrophe bond and ILS transaction

included in the data in this report please visit www.artemis.bm/deal_directory/

2013

2012

2011

2010

2009

2008

2007

2006

2005

2004

2003

2002

2001

2000

1999

1998

1997

+

�

17) A Leader in Collateral Trustee and

Insurance Linked Securities Services

As a leading provider of trust and agency services, we have the Collateral Trustee

and CAT Bond administration expertise to help reinsurers and the sponsors of

Insurance Linked Securities (ILS) meet their alternative capital funding needs.

We act as collateral trustee and in various agency capacities to deliver product

solutions for insurance and reinsurance companies, and support a wide range of

ILS activity, including Collateralized Reinsurance, Catastrophe Bonds, Industry

Loss Warranties (ILW), Sidecars, and ILS Fund Structures.

For more than 230 years, we have been a strong stable company with

excellent long-term credit ratings. BNY Mellon is the right choice for you.

For more information, please contact

Robert Thorson at 212-815-7149

bnymellon.com/corporatetrust

© 2015 The Bank of New York Mellon Corporation. All rights reserved. BNY Mellon is the corporate brand for The Bank of New York Mellon

Corporation. Products and services referred to herein are provided by The Bank of New York Mellon Corporation and its subsidiaries. Content

is provided for informational purposes only and is not intended to provide authoritative ï¬nancial, legal, regulatory or other professional advice.

For more disclosures, see https://www.bnymellon.com/us/en/disclaimers/business-disclaimers.jsp#corporatetrust

�

18) All catastrophe bond and ILS issuance data sourced

from the Artemis Deal Directory.

Opportunities exist to work with Artemis to increase your

profile to this segment of the global reinsurance and risk

transfer market. Advertising opportunities, sponsorship,

content development and partnership opportunities are

available. Contact us to discuss.

CONTACT ARTEMIS:

Steve Evans, Owner/Editor

steve@artemis.bm

+44 (0) 7711 244697

To download a media pack visit:

www.artemis.bm/advertise/

Copyright 2014 Artemis.bm, owned by Steve Evans Ltd.

�