1) the dti’s

Special Economic Zones

Tax Incentive Guide

towards full-scale industrialisation and inclusive growth

�

2) �

3) the dti’s Special Economic Zones Tax Incentive Guide

PREAMBLE

The South African Government established the Industrial Development Zones (IDZs)

programme in an effort to reposition itself in the world economy. The programme’s

main focus was to attract foreign direct investment (FDI) and the export of value-added

commodities. Although the IDZs recorded major achievements, there were weaknesses

that led to the policy review and the new Special Economic Zones (SEZs) policy.

The policy review and the new SEZ programme, which began in 2007, was also

brought about by developments in national economic policies and strategies, such as

the National Industrial Policy Framework (NIPF), National Devlopment Plan (NDP)

and the New Growth Path (NGP), as well as developments in the global economic

environment, such as the formation of BRICS (Brazil, Russia, India, China and South

Africa).

PURPOSE OF THE SEZ PROGRAMME

The new SEZ Policy provides a clear framework for the development, operation and

management of SEZs and addresses the challenges of the IDZ Programme.

The purpose of the SEZ programme is to:

• Expand the focus of strategic industrialisation to cover diverse regional

development needs and context;

• Provide a clear, predictable and systemic planning framework for the

development of a wider array of SEZs to support industrial policy objectives,

the Industrial Policy Action Plan (IPAP), NDP and the NGP;

• Clarify and strengthen governance arrangements, and expand the range and

quality of support measures beyond the provision of infrastructure; and

• Provide a framework for predictable financing to enable long-term planning.

�

4) PROGRAMME DESCRIPTION

The SEZ Act No. 16 of 2014 provides for:

• The designation, promotion, development, operation and management of SEZs;

• The establishment of the SEZ Advisory Board and the SEZ Fund;

• The regulation of application, issuing, suspension, withdrawal and transfer of SEZ

operator permits and the functions of SEZ operators;

• The transitioning of all current IDZs into SEZ status under specific guidelines;

• Determination of the SEZ Policy and Strategy;

• Enactment of regulatory measures and incentives for SEZs to attract domestic

investment and FDI; and

• Establishment of a One-Stop-Shop (OSS) to deliver government services within a

zone.

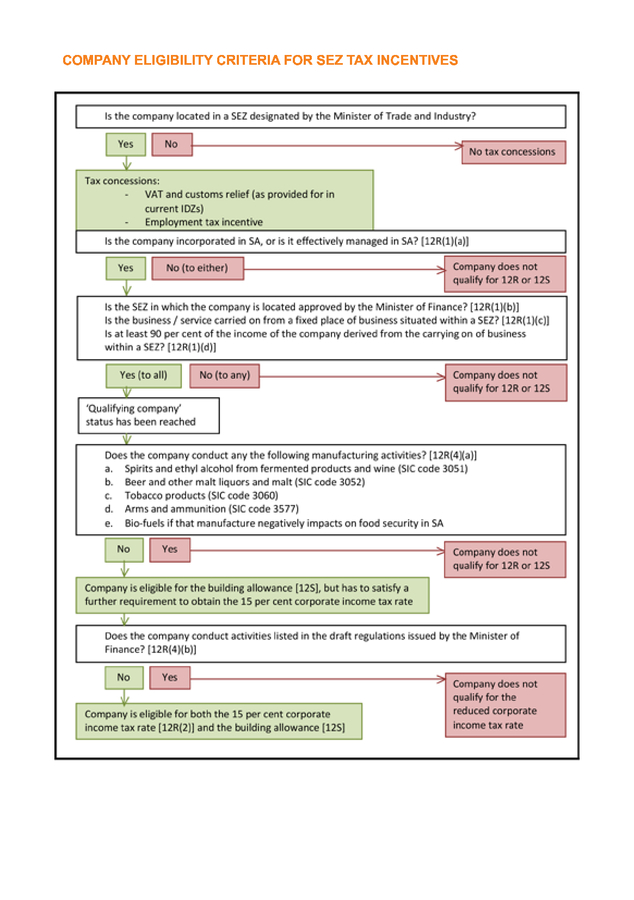

SEZ TAX INCENTIVES

To complement the Department of Trade and Industry’s (the dti’s) SEZ strategy, a

package of tax incentives will be available to qualifying companies locating in approved

SEZs, subject to certain criteria.

The tax incentives for qualifying companies include: VAT and customs relief, if located

within a customs-controlled Area (CCA); the employment tax incentive; building

allowance; and reduced corporate income tax rate.

The design and eligibility criteria for each incentive seeks to strike a balance between

achieving the objectives of higher levels of investment, growth and employment

creation, and ensuring that incentives are appropriately targeted for efficiency

purposes, while minimising any deadweight loss to the fiscus.

Qualifying businesses located within a CCA will qualify for VAT and customs relief

(similar to that for the current IDZs). The employment tax incentive will be available to

businesses located in any SEZ. Businesses operating within approved SEZs (approval

granted by the Minister of Finance, after consultation with the Minister of Trade and

Industry) will be eligible for two additional tax incentives. Firstly, all such businesses

can claim accelerated depreciation allowances on capital structures (buildings) and,

secondly, certain companies (carrying on qualifying activities within an approved SEZ)

will benefit from a reduced corporate tax rate (i.e. 15% instead of 28%).

�

5) VAT and Customs Relief

Companies located within a CCA will be eligible for VAT and customs relief per the

current VAT and customs legislation.

Characteristics of a CCA include:

• Import duty rebate and VAT exemption on imports of production-related raw

materials, including machinery and assets, to be used in production with the aim

of exporting the finished products;

• VAT suspension under specific conditions for supplies procured in South Africa;

and

• Efficient and expedited customs administration.

More information on CCAs can be found on the SARS website (www.sars.gov.za).

�

6) Employment Tax Incentive (ETI)

All employers employing low-salaried employees (below R60 000 per annum) in any

SEZ will be entitled to the employment tax incentive. This is an incentive aimed at

encouraging employers to hire young and less experienced work seekers. However,

the employee age restriction will not apply for SEZs. It reduces an employer’s cost of

hiring people through a cost-sharing mechanism with Government, while leaving the

wage the employee receives unaffected. The employer can claim the ETI and reduce

the amount of Pay-As-You-Earn (PAYE) tax payable by the amount of the total ETI

calculated in respect of all qualifying employees.

The employment tax incentive guide can be found on the SARS website.

�

7) Building Allowance

Qualifying businesses operating within approved SEZs (by the Minister of Finance,

after consultation with the Minister of Trade and Industry) will be eligible for an

accelerated depreciation allowance on capital structures (buildings). The special rate

of capital (depreciation) allowances in lieu of normal allowances will be available for

erecting or improving buildings and other fixed structures. This rate will equal 10% per

annum over 10 years.

Companies engaged in the following activities, based on the Standard Industrial

Classification (SIC) code issued by Statistics South Africa, will not qualify for the

building allowance:

• Spirits and ethyl alcohol from fermented products and wine (SIC code

3051)

• Beer and other malt liquors and malt (SIC code 3052)

• Tobacco products (SIC code 3060)

• Arms and ammunition (SIC code 3577)

• Bio-fuels, if their manufacture negatively impacts food security in South

Africa

�

8) Reduced Corporate Income Tax Rate

Certain companies will qualify for a reduced corporate income tax rate of 15% for the

period 2014-2024, instead of the current 28% headline rate. To qualify, the following

conditions must be met:

• The company must be located in a SEZ that is approved by the Minister of

Finance (in consultation with the Minister of Trade and Industry);

• It must be incorporated or effectively managed in South Africa;

• At least 90% of the income must be derived from the carrying on of business

or provision of services within that SEZ; and

• The company must not be engaging in the following activities, based on the

SIC code issued by Statistics South Africa:

*

Spirits and ethyl alcohol from fermented products and wine (SIC code

3051)

*

Beer and other malt liquors and malt (SIC code 3052)

*

Tobacco products (SIC code 3060)

*

Arms and ammunition (SIC code 3577)

*

Bio-fuels if that manufacture negatively impacts on food security in SA

*

MAJOR DIVISION 6: WHOLESALE AND RETAIL TRADE; REPAIR

OF MOTOR VEHICLES, MOTOR CYCLES AND PERSONAL AND

HOUSEHOLD GOODS; HOTELS AND RESTAURANTS

- Division 61: Wholesale and commission trade, except of motor

vehicles and motor cycles

- Division 62: Retail trade, except of motor vehicles and motor

cycles; repair of personal household goods

- Division 63: Sale, maintenance and repair of motor vehicles and

motor cycles; retail trade in automotive fuel

- Division 64: Hotels and restaurants

*

MAJOR DIVISION 7: TRANSPORT, STORAGE AND

COMMUNICATION

- Division 71: Land transport; transport via pipelines

- Division 72: Water transport

- Division 73: Air transport

- Division 74: Supporting and auxiliary transport activities; activities

of travel agencies

- Division 75: Post and telecommunications

*

MAJOR DIVISION 8: FINANCIAL INTERMEDIATION, INSURANCE,

REAL ESTATE AND BUSINESS SERVICES

- Division 81: Financial intermediation, except insurance and

pension funding

�

9) -

-

-

-

-

-

-

Division 82: Insurance and pension funding, except compulsory

social security

Division 83: Activities auxiliary to financial intermediation

Division 84: Real estate activities

Division 85: Renting of machinery and equipment, without

operator, and of personal and household goods

Division 86: Computer and related activities

Division 87: Research and development

Division 88: Other business activities

To assist companies in determining whether they are eligible for the tax incentives, the

following decision tree (eligibility criteria) can be used:

�

10) COMPANY ELIGIBILITY CRITERIA FOR SEZ TAX INCENTIVES

�

11) OTHER BENEFITS OF INVESTING IN AN SEZ

12i Tax Allowance Incentive

The 12I Tax Allowance Incentive is designed to support Greenfield investments (i.e.

new industrial projects that utilise only new and unused manufacturing assets) as well

as Brownfield investments (i.e. expansions or upgrades of existing industrial projects).

The new incentive offers support for both capital investment and training. For further

information, see http://www.thedti.gov.za/financial_assistance/financial_incentive.

jsp?id=45&subthemeid=26 or contact SEZenquiries@thedti.gov.za

One-Stop-Shop Facility

the dti is currently in the process of rolling out a One-Stop-Shop concept to the existing

IDZs in South African SEZs. In consultation with the key relevant national stakeholders,

the Minister of Trade and Industry will be entering into an Implementation Protocol for

the successful co-ordination of these relevant functions.

The aim of the SEZ One-Stop-Shop Facility will be to:

• Facilitate access by investors to all required permits and licences and other

informational requirements in a timely manner;

• Eliminate steps in the approvals/administrative process and allow parallel

rather than sequential approvals.

Key features of the One-Stop-Shop include:

• Physical Planning – Helps investors with planning of development of the

zones;

• Licensing – Simplifies process of obtaining business licences;

• Utilities – Facilitates a single point access to basic utilities required for setting

up operating industrial zone and other establishments;

• Industrial development incentives – Assists current and potential future

tenants to understand and access the portfolio of sector-specific incentives

and support measures available;

• Financing – Facilitates access of investors to direct or indirect financial

assistance to set up their business in the zones; and

• Environmental compliance – Assists in maintaining environmental standards

and obtaining environmental approvals.

For further information on the progress and launching of the Pilot OSS Facility, you are

welcome to contact the dti at SEZenquiries@thedti.gov.za

�

12) SEZ Fund For SEZ Infrastructure Development

Given longer term funding constraints, the SEZ Act and SEZ Policy encourage the

private sector to play an active role in the SEZ Programme. The SEZ Act envisages

both public and public-private partnerships (PPPs) in the development and operation of

SEZs.

This offers the potential for a number of different models involving:

• Assembly of land parcels with secure title and development rights by the

Government for lease to private zone development groups;

• Build-operate-transfer approaches to onsite zone infrastructure and facilities

with Government guarantees and/or financial support; and

• Contracting private management for Government-owned zones or lease of

Government-owned assets by a private operator.

An SEZ fund intends providing multi-year funding for SEZ infrastructure and related

operator performance improvement initiatives aimed at accelerating the growth of

manufacturing and internationally traded service operations, to be located within the

designated zones.

Industrial infrastructure is expected to leverage FDI and private investment and achieve

the following:

• Increased exports of value-added products;

• Measurable improvement in levels of localisation and related value chains;

• Increased beneficiation of mineral and agricultural resources;

• Increased flow of FDI;

• Increased job opportunities; and

• Creation of industrial hubs clusters and value chains in underdeveloped

areas.

The SEZ Fund will be available for pre- and post-designation to:

• Applicants currently operating with a valid operator permit, subject to

confirmation that an investor that requires infrastructure support has been

signed and the investment is in line with the programme objectives;

• Applicants in the process of setting up an SEZ subject to submission of a

comprehensive business/concept proposal determining clear socio-economic

benefits;

• Applicants that are licensees in terms of Chapter 5 of the SEZ Act;

• SEZ operators in terms of the SEZ Act; and

• A registered entity in South Africa in terms of the Companies Act.

�

13) The SEZ Fund is effective from 1 July 2013 to 31 March 2023.

For other industrial development Incentives and financial assistance offered by the dti

and International Trade Administration Commission of South Africa (ITAC), please visit

the dti website under the heading “Financial Assistance”.

�

14) �

15) To register as a SEZ stakeholder on the SEZ database, kindly complete the

stakeholder form on the dti website and e-mail to:

Ms Lizzy Mashiloane

Assistant Director: Special Economic Zones Stakeholder Management

Tel: +27 (0)12 394 1183

Fax: +27 (0)12 394 2183

E-mail: LMashiloane@thedti.gov.za

�

16) The Department of Trade and industry (the dti)

Address:

the dti Campus

77 Meintjies Street

Sunnyside

Pretoria

0002

South Africa

Website: www.thedti.gov.za

the dti Customer Contact Centre:

National: 0861 843 384

International: +27 12 394 9500

towards full-scale industrialisation and inclusive growth

�